DMA of 2026 MARCH 30 MONDAY AMC.

Stocks opened with broad gains following Friday’s sharp sell-off and a relatively quiet weekend on the Iran front. However, the major averages were unable to hold most of those gains amid pronounced weakness in semiconductor stocks and another day of sharply higher oil prices, ultimately leading to a mostly lower finish.

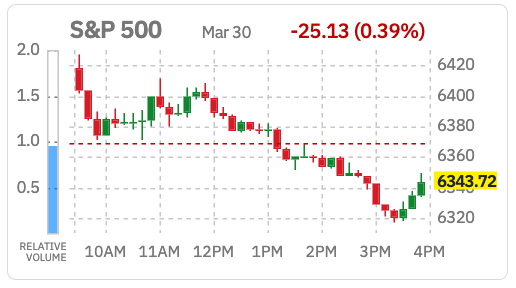

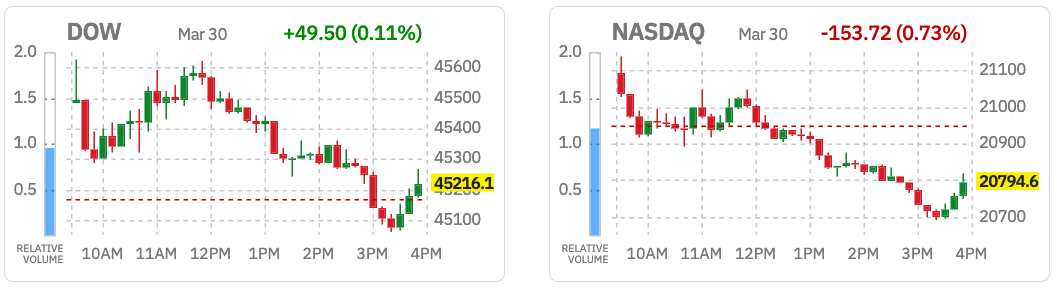

The Nasdaq Composite (-0.7%) lagged for most of the session amid the weakness in tech names, while the S&P 500 (-0.4%) moved lower in the afternoon, and strength in the broader market helped the DJIA (+0.1%) squeak out a modest gain. The smaller-cap Russell 2000 (-1.5%) and S&P Mid Cap 400 (-0.8%) moved lower earlier in the session, and finished with wider losses.

Much of the early strength in equities was attributed to a technical bounce in the wake of Friday’s sell-off. All eleven S&P 500 sectors traded higher out of the gate, but losses across tech names quickly capped gains at the index level.

The top-weighted information technology sector (-1.5%) was one of the first S&P 500 sectors to move into negative territory as semiconductor stocks saw an extension of recent weakness. The PHLX Semiconductor Index finished 4.2% lower as names such as Micron (MU 321.80, -35.42, -9.92%) and Coherent (COHR 219.65, -23.83, -9.79%) were among the worst-performing S&P 500 names today.

It is worth noting that losses in the broader technology sector were somewhat lessened due to a strong showing from software stocks that sent the iShares GS Software ETF (IGV) 1.0% higher. ServiceNow (NOW 104.97, +5.56, +5.59%) was the top-performing S&P 500 component while Palo Alto Networks (PANW 154.35, +7.33, +4.99%) captured a similar gain after disclosing that its CEO purchased approximately $10 million worth of shares late Friday.

The industrials sector (-1.6%) was also a laggard today, while the energy sector (-0.9%) also finished lower despite crude oil futures settling today’s session $3.41 higher (+3.4%) at $102.92 per barrel.

There was some early optimism on the geopolitical front after President Trump wrote on Truth Social that Iran has conceded most of the demands in the 15-point peace proposal that the U.S. set forth, though he did not provide details. Additionally, the same post included threats to destroy Iran’s energy infrastructure if a deal is not struck soon. A lack of clarity and climbing oil prices kept the market’s enthusiasm in check, while reports circulated late in the session that Israel’s Air Force completed a wave of attacks on infrastructure sites in Tehran, suggesting a resolution remains distant.

However, the market received some encouraging news today regarding the Fed’s view of the situation in Iran. Fed Chair Jerome Powell (voting FOMC member) said inflation expectations remain well anchored beyond the short term and noted that the Fed’s tools do not have a meaningful impact on supply shocks. This commentary had a notable impact on market-implied rate expectations, with the probability of a rate hike later this year falling to around 5% from over 20% on Friday, according to the CME FedWatch Tool.

Corporate news flow was on the lighter side today, though there were a few notable moves. Sysco (SYY 69.30, -12.50, -15.28%) was the worst-performing S&P 500 component after agreeing to acquire Jetro Restaurant Depot in a $29.1 billion deal.

With tomorrow marking the final trading day of the quarter, positioning dynamics could come into focus. However, the major averages remain firmly below their 200-day moving averages, highlighting a still-challenged technical backdrop as oil prices continue to climb.

Unlike stocks, U.S. Treasuries began the week with strong gains across the curve, bouncing off their lowest levels of the month ahead of tomorrow’s final session of Q1. The 2-year note yield settled down nine basis points to 3.83%, and the 10-year note yield settled down 10 basis points to 4.34%.

There was no economic data of note.

BENCHMARK INDICES YEAR-TO-DATE

- S&P Mid Cap 400: -0.7% YTD

- Russell 2000: -2.7% YTD

- DJIA: -5.9% YTD

- S&P 500: -7.3% YTD

- Nasdaq Composite: -10.5% YTD

MARKET INTERNALS

- DOW closed higher at 45216 (+0.11%).

- Nasdaq closed lower at 20795 (-0.73%).

- S&P 500 closed lower at 6344 (-0.39%).

- Action came on lower than average volume for NYSE but higher for Nasdaq (NYSE 1,379 mln vs avg. of 1,431 mln; NASDAQ 9,316 mln vs avg. of 9,097 mln),

- Advancing/declining volume for NYSE (650 mln/702 mln) and Nasdaq (4153 mln/5125 mln).

- Decliners led advancers (NYSE 1367/1392; NASDAQ 2027/2807)

- New 52-week lows outpacing new 52-week highs (NYSE 90/168, NASDAQ 53/534).

After-Hours Action

US stock indices were mixed on a volatile Monday as a sharp retreat in Treasury yields failed to sustain a broad based equity rally following dovish remarks from Federal Reserve Chair Jerome Powell. While the Dow edged 0.1% higher, the S&P 500 and Nasdaq Composite dipped 0.4% and 0.8% respectively as heavy losses in the semiconductor sector offset gains in financials and utilities. Powell signaled that the central bank intends to look through the current energy price shock with West Texas Intermediate futures surging amid persistent threats to Red Sea exports and Iranian infrastructure. Although the 10-year Treasury yield tumbled, chipmakers like Micron (-9.7%) and Lam Research (-5.4%) led the decline as investors pivoted toward energy and utility giants reaching all time highs. Despite President Trump’s report of serious discussions in Iran the CBOE Volatility Index remained elevated as markets weigh resilient corporate earnings against the risk of an energy infrastructure meltdown.

After Hours Gainers:

Companies trading higher in after hours in reaction to earnings/guidance: SPCE +14.7%, PRGS +1.5%

Companies trading higher in after hours in reaction to news: MKC +2.3% (Unilever PLC nearing deal to form $60 bln food company with McCormick (MKC), according to WSJ), UL +1.6% (Unilever PLC nearing deal to form $60 bln food company with McCormick (MKC), according to WSJ), ARRY +1.5% (opening of the new headquarters of APA Solar), RKLB +0.5% (receives regulatory approval to acquire Mynaric), SPIR +0.3% (launches ten satellites aboard SpaceX’s Transporter-1), AXP +0.2% (named official payments partner of the NFL), STNG +0.1% (to sell two 2015 built scrubber-fitted MR product tankers for $35 mln per vessel), SLF +0.1% (completes remaining equity interest purchases of BGO and Crescent Capital)

After Hours Losers:

Companies trading lower in after hours in reaction to earnings/guidance: PHR -21.3%

Companies trading lower in after hours in reaction to news: PEPG -48% (topline results from lowest dose (5 mg/kg) MAD cohort in the ongoing Phase 2 FREEDOM2 Study), SVC -16.8% (stock offering), PALI -5.6% (topline data from phase 1b clinical study of PALI-2108), VRT -0.5% (to invest $50 mln to expand manufacturing presence in Ohio), FDS -0.3% (strategic partnership with Finster AI to power new AI banking platform), NFLX -0.2% (looking to expand its NFL package to four games, according to WSJ)

BONDS AND YIELDS

U.S. Treasuries began the week with strong gains across the curve, bouncing off their lowest levels of the month ahead of tomorrow’s final session of Q1. Treasuries were off to firmly higher start after a night that saw stellar gains in other sovereign debt. Longer-dated JGBs diverged from the global trend, retreating after the latest Summary of Opinions from the Bank of Japan did not show opposition to additional rate hikes. As for Iran, the situation changed little over the weekend, which was encouraging for the moment, though an elevated sense of uncertainty remains in place. Treasuries added to their starting gains in morning trade, reaching highs in the early afternoon. There was some light backtracking during the final hour, but it only lifted the 10-yr yield by two basis points off its low. Crude oil headed back above $100/bbl while the U.S. Dollar Index climbed 0.3% to 100.47, briefly touching its highest level since May.

Yields

- 2-yr: -9 bps to 3.83%

- 3-yr: -8 bps to 3.86%

- 5-yr: -9 bps to 3.98%

- 10-yr: -10 bps to 4.34%

- 30-yr: -8 bps to 4.91%

CURRENCIES

The US dollar index rose past 100 on Monday, its highest since May of last year as no signs of de-escalation to the war in the Middle East maintained markets’ preference to holding safety through the greenback. Yemeni Houthis engaged in the conflict over the weekend to threaten exports through the Red Sea, while President Trump issued new warnings to Tehran after Iranian speakers repeatedly touted US demands as unrealistic. Crude oil and fuel prices maintained their surge from the month, supporting the outlook for a hawkish response by the Federal Reserve. The Fed was due to hold its rates unchanged next month as leading labor market indicators reflected a robust labor market, while private surveys indicated higher energy costs being faced by manufacturers. The increase in energy prices also support the dollar as a safe-haven instead of the yen and the franc due to the US being a major energy exporter, in addition to forcing importers in buying more dollars for oil and LNG.

Currencies

- EUR/USD: -0.4% to 1.1459

- GBP/USD: -0.6% to 1.3183

- USD/CNH: UNCH at 6.9164

- USD/JPY: -0.4% to 159.64

Euro Set to End March 2% Weaker

The euro slipped to $1.15 by the end of March, flirting with its weakest level since mid-March and heading for a monthly drop of over 2% against the dollar. Risk aversion intensified as traders weighed the economic fallout from the worsening Middle East conflict, with reports of US troop preparations for a possible ground operation eclipsing Washington’s claims of progress in Iran talks. Economic data added to the pressure: German CPI pointed to rising inflation in Europe’s largest economy, while the Eurozone business survey showed a steep decline in sentiment as inflation expectations spiked. Markets have radically repriced ECB policy, now anticipating at least two rate hikes in 2026, and potentially a third, ditching earlier expectations of a 40% chance of a cut. Meanwhile, French central bank chief François Villeroy de Galhau stressed the ECB’s resolve to contain energy-driven inflation, though he cautioned it was “too early” to discuss specific timing for rate increases.

Sterling Nears 1% Monthly Drop on Middle East Jitters

The British pound drifted toward $1.32, lingering near its lowest since early December and on track for a monthly decline of over 1% against the US dollar. Risk aversion dominated markets as traders assessed the economic risks from the protracted Middle East conflict, with reports of US troop preparations for a potential ground operation overshadowing Washington’s claims of progress in Iran negotiations. Meanwhile, Bank of England policy expectations underwent a dramatic shift: markets now anticipate at least two rate hikes in 2026, with a possible third, reversing earlier bets on two cuts. Meanwhile, BoE policymaker Alan Taylor struck a cautious tone last week. He emphasized a “high bar” for rate increases, advocating to hold borrowing costs steady until the economic impact of the Iran conflict becomes clearer.

Offshore Yuan Edges Higher

The offshore yuan edged higher to around 6.91 per dollar on Monday, trimming losses from the previous week despite subdued market sentiment amid escalating tensions in the Middle East. The US–Israel confrontation with Iran has thrown the region into turmoil, with the Strait of Hormuz, a key artery for global trade, effectively closed and threatened major energy facilities. However, China appears largely insulated from the crisis, holding substantial energy reserves and having invested heavily in alternative energy sources. Still, the yuan is expected to weaken in the near term, as ongoing conflict pushes oil prices higher and bolsters demand for the US dollar. On the trade front, Beijing has launched investigations into US trade practices in response to earlier probes by the Trump administration. This move follows the White House’s confirmation that Trump was scheduled to travel to China in mid-May for a long-awaited summit with President Xi Jinping.

Aussie Extends Losing Streak

The Australian dollar weakened further to around $0.685, down for a seventh straight session to hit its lowest since January 23 as a sharp rise in energy prices amid ongoing Middle East tensions clouded the global economic outlook and pushed investors toward the safety of the US dollar. The Aussie also fell 2.1% last week, its worst weekly performance since April, and is now on track for a roughly 3.8% monthly decline, the steepest since December 2024. Oil prices continued to climb as the conflict in Iran entered its fifth week, with renewed attacks in the region increasing risks to global energy supply. In response, Australia’s Prime Minister Anthony Albanese announced a temporary cut to fuel taxes to help ease cost pressures, underscoring the broader impact of rising energy prices on the economy. Focus now turns to the release of the RBA’s latest meeting minutes after a narrow vote to lift rates to 4.1%, as policymakers balance persistent inflation against a softening growth outlook.

COMMODITIES

WTI crude oil futures rose to $101.7 a barrel and Brent crude oil futures were volatile near $112 a barrel on Monday, poised for a record monthly surge of more than 50% in March, as the ongoing Middle East conflict continues to disrupt energy markets. President Donald Trump threatened attacks on Iran’s energy infrastructure, overshadowing his remarks that a deal to end the hostilities could be near. Trump warned that if no agreement is reached soon and the Strait of Hormuz is not “immediately ‘Open for Business,’” the US could target Iran’s power plants, oil wells, and Kharg Island. Prices had already climbed earlier in the session following the deployment of additional US troops and the involvement of Yemen’s Iran-backed Houthis in the conflict. The war has nearly halted traffic through the Strait of Hormuz, with traders warning of further energy price spikes if the fighting continues.

The spread between Brent and WTI is currently at $8.96

Commodities

- Crude Oil +3.41 @ 102.92

- Nat Gas -0.14 @ 2.89

- Gold +64.20 @ 4557.00

- Silver +0.86 @ 70.63

- Copper unchanged @ 5.50

Gasoline Extends Momentum

US gasoline futures rose above $3.35 per gallon, hitting their highest level since July 2022 as the effective closure of the Strait of Hormuz continues to choke global supply and drive a record 30% monthly gain. This price surge is underpinned by the physical disruption of critical energy corridors where Houthi involvement in Yemen has introduced fresh risks to Red Sea transit and Yanbu shipments. While President Trump hinted at serious discussions to end the five-week conflict his concurrent ultimatum to obliterate Iranian power plants and the Kharg Island export hub if the waterway remains blocked has reinforced a massive geopolitical risk premium. The deployment of additional US forces and the resulting spike in WTI crude have created a floor that outweighs the impact of deteriorating global growth prospects. Consequently gasoline remains tethered to these supply-side shocks as the market weighs the hope of a peace deal against the threat of energy infrastructure destruction.

Heating Oil Hovers Between Gains and Losses

Heating oil futures oscillated near $4.5 per gallon as the physical displacement of roughly 20% of global oil transit continues to paralyze the distribution of middle distillates. This supply-side crisis is driven by the near-total shutdown of the Strait of Hormuz and fresh Houthi threats to Red Sea shipping which have forced global inventories down to critical levels. While tentative signals of a diplomatic breakthrough in the five-week Middle East conflict offer a potential ceiling the rally remains anchored by a massive risk premium following President Trump’s ultimatum to target Iranian export hubs. The arrival of 10,000 additional US troops and the grounding of vessels in key waterways have created a price floor that outweighs the dampening effect of high financing costs and growth prospects. Consequently, heating oil remains tethered to WTI crude as the market awaits confirmation of a peace deal before pricing out the threat of total energy infrastructure destruction.

Urals Oil Rises to 13-Year High

Russian Urals crude jumped to around $110 per barrel, the highest since 2013, as global oil prices climbed amid the ongoing Middle East conflict. Disruptions to Gulf supplies through the Strait of Hormuz have pushed crude above $100, with Russia benefiting as buyers seek alternative sources. President Donald Trump said he expects to reach a deal to end hostilities but also threatened strikes on Iran’s energy infrastructure, including Kharg Island, warning that if the strait is not reopened, the US could target oil and power facilities. President Vladimir Putin urged Russian producers to capitalize on soaring prices but cautioned that the surge is temporary. Meanwhile, the US expanded a permit allowing countries to purchase Russian crude, extending a temporary waiver previously granted only to India. Indian refiners, including Indian Oil Corp. and Reliance Industries, have bought around 30 million barrels of Russian crude after receiving approval in early March, according to sources.

Silver Rises Above $70.5

Silver prices rose above $70.5 per ounce on Monday as the market balanced tentative optimism regarding a diplomatic resolution in Iran against the persistent threat of physical supply shortages and Houthi activity in the Red Sea. While President Trump cited serious discussions with a more reasonable regime to end the five-week conflict, silver remains sensitive to his warning that failure to reopen the Strait of Hormuz will lead to the obliteration of Iranian infrastructure. Despite the rebound the metal remains nearly 30% below its March peak as the energy shock to $115 Brent crude continues to stoke global inflation concerns and limit policy flexibility. A strengthening US dollar further caps gains by increasing costs for overseas buyers while investors pivot toward Treasuries as growth concerns from potential shortages begin to manifest. As the market awaits key US jobs data the trajectory for silver hinges on the current peace plan’s success.

Gold Holds Small Gains

Gold traded above $4,510 per ounce on Monday as the market balanced tentative hopes for a diplomatic resolution against the persistent inflationary risks of a prolonged energy shock. While President Trump cited serious discussions with a more reasonable regime in Iran, Bullion remains sensitive to his concurrent threat to obliterate Iranian oil and power infrastructure if a deal is not reached shortly. Despite these headlines, gold is down more than 15% from its March peak as Brent crude climbing above $115 reinforces expectations that higher energy costs will limit the Federal Reserve’s room for aggressive rate cuts. Furthermore a firmer US dollar and a rebound in Treasuries have dampened the appeal of non-yielding assets even as Houthi attacks in the Red Sea sustain a high geopolitical risk premium. As investors weigh El-Erian’s warnings of limited policy flexibility the metal’s trajectory remains tethered to the outcome of these high-stakes negotiations.

Arabica Coffee Futures at Over 2-Week Low

Arabica coffee futures eased to near $2.9 per pound, the lowest in over two weeks, pressured by expectations of increased global supply, especially from top producer Brazil. The start of the harvest in the coming weeks is expected to gradually increase the availability of coffee in the physical market, which reinforces seasonal pressure on prices. On Thursday, Marex Group Plc projected a record 2026/27 Brazil coffee crop of 75.9 million bags, surpassing last week’s forecast from Sucafina of 75.4 million bags, and representing a 15.5% year-on-year increase. Earlier this month, StoneX also raised its Brazil 2026/27 production estimate to a record 75.3 million bags, up from 70.7 million bags in November. At the same time, certified Arabica stocks have picked up recently, though still below historical norms, providing some relief to near-term supply pressures. Meanwhile, the market remains alert as Middle East tensions push oil prices higher, boosting transportation and operational costs.

UK Natural Gas Futures Edge Up

UK natural gas futures edged up to around 138 pence per therm as supply risks countered softer demand. er to around €55 per MWh as supply risks offset weaker demand, with geopolitical tensions remaining in focus. President Donald Trump said a deal to end military operations in Iran is likely but warned of major strikes on key infrastructure including Kharg Island if the Strait of Hormuz is not reopened. About a fifth of global LNG normally passes through the Strait of Hormuz, but traffic has nearly halted since strikes on Iran began on February 28. With little sign of de-escalation, geopolitical tensions continue to support prices despite weaker near-term fundamentals. Gains remain limited as Europe benefits from stronger wind generation and milder temperatures, which are expected to reduce power sector demand in early April. Still, UK gas prices have surged roughly 75% over March, reflecting ongoing strain in energy markets as the blocked strait disrupts key supply routes.

Steel Rises on Supply Disruptions

Steel rebar futures rose toward CNY 3,140 per ton, recouping losses from last week as supply constraints linked to the Iran war lifted fuel and shipping costs, keeping a risk premium on prices. Israel also struck two major steel factories in Iran reportedly tied to the IRGC, adding further complexity to the global steel market. In China, recent data showed steel production fell 3.6% to 76.1 million tons in February, while global output declined 2.2% to 141.8 million tons. During the annual parliamentary sessions in Beijing earlier this month, authorities reaffirmed their commitment to reducing overcapacity in the steel sector amid weakening demand. China’s steel industry continues to face structural headwinds as the economy matures, with softer construction activity further pressured by the prolonged property downturn.

Copper Remains Under Pressure

Copper held below $5.5 per pound on Monday, struggling for traction as investors navigated ongoing hostilities in the Middle East that showed no signs of easing. Tensions escalated as Iran-backed Houthi militants in Yemen joined the conflict, targeting Israel over the weekend. President Donald Trump also said he could “take the oil in Iran,” echoing the US military operation in Venezuela earlier this year. Copper and other industrial metals have come under pressure this month as disruptions from the conflict and surging energy prices heightened concerns over inflation and slowing global industrial activity. Upward price pressures have also reinforced expectations that major central banks may raise interest rates this year, with markets now pricing in a potential rate increase from the Federal Reserve, a sharp reversal from earlier expectations for two rate cuts.

Baltic Dry Index Snaps 3-Day Advance

The Baltic Exchange’s dry bulk freight index, which monitors rates for ships carrying dry bulk commodities, snapped a three-day winning streak on Monday, falling about 0.7% to 2,017 points. The capesize index, which typically transport 150,000-ton cargoes including iron ore and coal, decreased by 0.9% to 3,004 points, after three consecutive sessions of gains; and the panamax index, which usually carry 60,000 to 70,000 tons of coal or grain, fell 0.8% to a near seven-week low of 1,742 points. Among smaller vessels, the supramax index eased 3 points, or 0.3%, to 1,203 points.

Palm Oil Market Stays Buoyant to Start Week

Malaysian palm oil futures extended gains for a third session on Monday, with prices holding above MYR 4,650 per tonne. A weaker ringgit underpinned sentiment, along with strength in Dalian palm olein as well as soyoil prices in Chicago markets. Robust exports added momentum, as cargo surveyors noted March 1–25 shipments surged 38–51% from February, reflecting strong post-Eid demand. Supply concerns also lent support, with top supplier Indonesia accelerating its B50 biodiesel rollout and weighing higher April export taxes. Crude oil’s upside amid the Iran war further bolstered sentiment. However, upside was capped by softer demand from top buyer India, where March imports are projected at 680,000 tonnes versus 847,689 tonnes in February. Indian regulators also extended the suspension of derivatives trading in key agricultural commodities, including crude palm oil, through March 2027. Caution lingered ahead of the March PMI data in China, another main consumer, set for later this week.

ROTW UPDATES

Equity indices in the Asia-Pacific region began the week on a mostly lower note with South Korea’s Kospi (-3.0%) and Japan’s Nikkei (-2.8%) leading to the downside.

- Japan’s Nikkei: -2.8%,

- Hong Kong’s Hang Seng: -0.9%,

- China’s Shanghai Composite: +0.2%,

- India’s Sensex: -2.2%,

- South Korea’s Kospi: -3.0%,

- Australia’s ASX All Ordinaries: -0.6%.

In news:

- There was little apparent change to the situation in the Middle East over the weekend, leaving some recent concerns in place.

- The Japanese yen briefly hit its lowest level against the dollar since mid-2024 before bouncing.

- The rebound followed the release of the Bank of Japan’s latest Summary of Opinions, which did not show opposition to additional rate hikes.

- There was an increase in expectations for a rate hike from the Reserve Bank of Australia.

- Companies listed in China and Hong Kong reported a 3.55% yr/yr increase in profits for fiscal 2025.

In economic data:

- India’s February Industrial Production 5.2% yr/yr (expected 4.7%; last 4.8%) and February Manufacturing Output 6.0% m/m (last 4.8%)

Major European indices trade in the green despite a continued rise in energy prices that has Brent crude approaching $110/bbl.

- STOXX Europe 600: +0.5%,

- Germany’s DAX: +0.2%,

- U.K.’s FTSE 100: +0.9%,

- France’s CAC 40: +0.3%,

- Italy’s FTSE MIB: +0.5%,

- Spain’s IBEX 35: +0.2%.

U.S. ECONOMIC UPDATES

US stock indices were mixed on a volatile Monday as a sharp retreat in Treasury yields failed to sustain a broad-based equity rally following dovish remarks from Federal Reserve Chair Jerome Powell. While the Dow edged 0.1% higher, the S&P 500 and Nasdaq Composite dipped 0.4% and 0.8% respectively as heavy losses in the semiconductor sector offset gains in financials and utilities. Powell signaled that the central bank intends to look through the current energy price shock with West Texas Intermediate futures surging amid persistent threats to Red Sea exports and Iranian infrastructure. Although the 10-year Treasury yield tumbled, chipmakers like Micron (-9.7%) and Lam Research (-5.4%) led the decline as investors pivoted toward energy and utility giants reaching all time highs. Despite President Trump’s report of serious discussions in Iran the CBOE Volatility Index remained elevated as markets weigh resilient corporate earnings against the risk of an energy infrastructure meltdown.

US Dallas Fed Manufacturing Index Falls in March

The Dallas Fed’s general business activity index for Texas manufacturing fell to -0.2 in March 2026 from 0.2 in February, indicating no change in activity. However, the company outlook index dropped nearly seven points to -3.5, moving into negative territory. The outlook uncertainty index surged 20 points to 26.0, its highest reading since April 2025. Employment growth stalled and workweeks were flat in March. The employment index came in near zero, with 15 percent of firms reporting net hiring and 16 percent reporting net layoffs. The hours worked index fell to 0.9 from 6.1. Price pressures were little changed while wage growth slowed. The finished goods prices index and raw materials prices index held relatively steady at 18.4 and 32.7. The wages and benefits index fell to 25.2 from 31.9. Looking ahead, manufacturers expect increased activity in six months. The future production index held steady at 35.7 and the future general business activity index fell two points to 10.6.

- President Trump confirms, ‘serious discussions with a new, and more reasonable, regime to end our Military Operations in Iran’. Truth Social

- President Trump says Iran has agreed to most demands. Bloomberg

- President Trump tells FT the US may take Iran’s oil

- President Trump speculates about seizing Kharg Island from Iran. The Independent

- President Trump speculates about seizing Iran’s uranium. WSJ

- President Trump said on Sunday that long sought after targets in Iran have been taken out

- Bond market underestimating slowdown risk, according to JPMorgan and PIMCO. Bloomberg

- Senate Banking Committee plans to complete nomination proceedings for the new Fed Chairman by April 13.

- The Japanese yen briefly hit its lowest level against the dollar since mid-2024 before bouncing. The rebound followed the release of the Bank of Japan’s latest Summary of Opinions, which did not show opposition to additional rate hikes.

- U.S. Treasury officials will reach out to domestic and international insurance regulators to discuss systemic risk within the private credit sector.

- India restricting speculative bets against rupee. Bloomberg

- Treasury Secretary Scott Bessent signals optimism on Strait of Hormuz reopening; says U.S. working to close global oil supply gap, Bloomberg citing Fox News interview

- U.S. deploys hundreds of special forces, Marines, and paratroopers to Middle East amid Strait of Hormuz tensions, according to CBS News

- US Department of Labor proposes landmark rule to democratize access to alternative investments in 401(k) plans

- Israeli Air Force confirms it has ‘completed a wave of extensive strikes a short while ago targeting infrastructure of the Iranian terror regime in the heart of Tehran’

trading econ

EARNINGS SEASON AND GUIDANCE

- Alaska Air (ALK) issues downside Q1 earnings guidance, unit revenue tracking in line with prior expectations

- Americas Silver (USAS) announces strong full-year 2025 results and 2026 guidance with ~30% annual production growth

- Aura Biosciences (AURA) reports Q4 results

- Bicara Therapeutics (BCAX) reports Q4 results

- CareCloud (CCLD) highlights preferred conversion progress, reaffirms growth outlook

- Eikon Therapeutics (EIKN) reports FY25 results, highlights $381 mln IPO and advances oncology pipeline with key Phase 2 enrollment completion

- Fermi America (FRMI) reports FY25 results

- Rezolve AI Limited (RZLV) delivers 543% H2 growth; raises 2026 revenue guidance to $360 mln as platform achieves global infrastructure scale

- Sigma Lithium (SGML) announces full year 2025 results: US$31 mln cash flow and 47% cash margin in 4Q25; signed US$146 mln in two offtake agreements

- Standard Lithium (SLI) reports fourth quarter results; Provides an update on plans for a Final Investment Decision on the South West Arkansas project

- Sysco (SYY) reaffirms FY26 outlook

- Turbo Energy (TURB) estimates 2025 revs +130-140%

- Unicycive Therapeutics (UNCY) announces full year 2025 financial results and provides business update

- USA Rare Earth (USAR) reports Q4 results

- Veradermics (MANE) reports Q4 results

- Xerox (XRX) CEO Steve Bandrowczak will step down, Board appointed Louie Pastor as new CEO effective immediately; reaffirms guidance

2026 MAR 31

Pre-Market: FRMI

After-Hours: PHR PRGS

THE WEEK AHEAD

WEEK 13: MONDAY TO FRIDAY, MARCH 30 to APRIL 03

According to the PTSD*, Week 14 has FOUR trading days and is the FIRST trading week in April 2026. The next Market Holiday is on FRIDAY APR03. Seasonally, Week 14 has a Bearish-to-Flat outlook, leading to a more positive Week 15. outlook with Risk-On sentiment, at least on the 15-year cycles. April is the last of the “6 months of bullishness” on the SPX.

We also need to keep in mind that with the current POTUS, seasonals can easily go out of whack.

*PTSD – Penguin Trader Seasonal Data.

BENCHMARK INDICES (21-YEAR AVERAGE)

The Stock Trader’s Almanac’s stats for the Benchmark Indices for 2026 MARCH 31 of Week 13 over a 21-year average are:

- Dow Jones (DJIA): Bullish 66.7%

- S&P 500 (SPX): Bullish 61.9%

- NASDAQ (COMP): Bullish 71.6%

- *Russells 2000 (RUT): 66.7%

*The RUT is not listed in the STA; several penguins with a slide ruler calculated the 21-year average.

BENCHMARK INDEX ETFs

The Penguin Trader Seasonal Data (PTSD) stats for the Benchmark Index ETFs for 2026 MARCH 31 of Week 13 over a 15-year average are:

- DIA – (15yr Avg): Bullish 73.3%

- SPY – (15yr Avg): Bullish 66.7%

- QQQ – (15yr Avg): Mildly Bullish 53.3%

- RUT – (15yr Avg): Bullish 60.0%

ECONOMIC DAY AHEAD

For USA’s upcoming economic calendar features:

- 9:00 ET: January FHFA Housing Price Index (Briefing.com consensus 0.0%; prior 0.1%) and January S&P Case-Shiller Home Price Index (Briefing.com consensus 1.3%; prior 1.4%)

- 9:45 ET: March Chicago PMI (Briefing.com consensus 54.8; prior 57.7)

- 10:00 ET: February Job Openings (Briefing.com consensus 6.795 mln; prior 6.946 mln) and March Consumer Confidence (Briefing.com consensus 88.0; prior 91.2)

ANALYSIS

A penguin will be volunteered for this post soon, or if incentivised with enough cheese.

COMMENTARY

Monday night. I just went to bed early. My body was physically too tired to consider performing any trades.

The war goes on, and the media reporting is so skewed, I seriously doubt the reporters believe what they are reporting, too. The VIX is at a high, we are still pretty bearish technically on the SPX, and the general read is that life in middle America is not.

China (save Taiwan) reported that businesses have more than 3% profits year on year; and for 20260331, both the STA’s (21-year) and the PTSD’s (15-year) seasonals are in line.

Over the weekend, I was blessed with Komputer Penguin, who helped me identify and resolve the linking issues that WordPress had with Facebook posts. Somehow, the links worked in normal browsers and even in FB Messenger, but not on the FB walls. I am also happy to have regular readers from the village tell me of the problem. Feedback is always welcome – as I said before, I actually do not know how many penguins actually read this blog; and receiving any form of encouragement is good for me.

Aside from the blog technicals. I also completed several experiments depositing funds into IB and TT using WISE, and transferring SGD to USD on IB.

— One more shout-out to my Penguin friend “D”, please contact me if you read this. Somehow, all of your emails have been bouncing.

Stay Hedged – My Penguin Friends

(Excerpts from briefing.com, tradingeconomics.com, financialscents.com, factset.com, finviz.com, marketwatch.com, etrade.com, yahoo.com, tigerbrokers.com, tradingview.com, tradingcentral.com, theedgemalaysia.com, sectorspdrs.com, Investopedia.com, and CNBC.com)