DMA of 2026 APRIL 21 TUESDAY AMC.

The stock market had a relatively busy day today, with a significant wave of earnings reports, continued geopolitical volatility, and a smattering of corporate headlines from some of the market’s largest companies giving investors plenty to assess. The market is also likely still digesting the scope of its recent push into record territory.

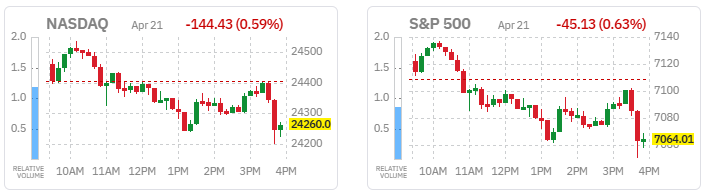

The S&P 500 (-0.6%), Nasdaq Composite (-0.6%), and DJIA (-0.6%) spent the first two hours or so of the session with solid gains before retreating as oil prices spiked amid reports that Iran may not send delegates to Pakistan for the next round of negotiations with the U.S. The 10-day ceasefire between the U.S. and Iran is set to expire tomorrow, adding a heightened sense of uncertainty to the situation as President Trump has threatened renewed strikes against Iran if a deal is not struck. The market moved to session lows in the final hour of trading after CNBC reported that Iran will not attend talks in Pakistan unless the U.S. “abandons its threats,” and The Associated Press reported Vice President JD Vance called off his trip to Pakistan, where he was set to lead the U.S. side of negotiations.

Crude oil futures settled today’s session $2.40 higher (+2.7%) at $91.80 per barrel, with the bump giving investors pause after the recent rally to record highs signaled that markets may have largely looked past the conflict or already priced in a path toward de-escalation.

Participation was weak in the broader market, with only the energy sector (+1.3%) finishing in positive territory. The sector was supported by the increase in oil prices and a nice move from Halliburton (HAL 38.15, +1.47, +4.01%) after the company beat earnings expectations.

The top-weighted information technology sector (-0.2%) was a relative outperformer, though it could not maintain its modest gain in the final hour of the session. Software names posted another winning session, with Microsoft (MSFT 424.16, +6.09, +1.46%) a mega-cap standout amid a weak showing for the market’s largest names, and the iShares GS Software ETF advancing 0.5%.

Those gains were largely offset by weakness in Apple (AAPL 266.17, -6.88, -2.52%) after the company announced CEO Tim Cook will step down, with John Ternus set to take his place on September 1. NVIDIA (NVDA 199.88, -2.18, -1.08%) also charted a lower course.

The consumer discretionary sector (-0.5%) also moved into negative territory late in the session. Amazon (AMZN 249.91, +1.63, +0.66%) notched a modest gain after announcing an expanded partnership with Anthropic, highlighted by a potential $25 billion incremental investment and a commitment from Anthropic to spend over $100 billion on AWS over the next decade.

Elsewhere in the sector, homebuilders moved higher after D.R. Horton (DHI 162.20, +8.86, +5.78%) turned in a solid earnings report, while Tractor Supply (TSCO 39.57, -5.24, -11.69%) was the worst-performing S&P 500 component after missing earnings estimates.

Earnings were a key driver of price action in the broader market, with most of today’s batch easily topping estimates. Northern Trust (NTRS 171.74, +12.75, +8.02%) was the best-performing S&P 500 component, while UnitedHealth (UNH 346.01, +22.53, +6.96%) was the top Dow component.

However, several notable names beat estimates but issued softer guidance, resulting in sharp retreats today. Northrop Grumman (NOC 611.13, -45.85, -6.98%) and GE Aerospace (GE 286.73, -16.87, -5.56%) were examples of this trend, which weighed heavily on the industrials sector (-1.4%).

Elsewhere, the real estate sector (-1.9%) faced the widest loss as treasury yields moved higher today.

Outside of the S&P 500, the smaller-cap Russell 2000 (-1.2%) and S&P Mid Cap 400 (-0.6%) followed a similar trajectory to the major averages.

All told, today’s session underscored the challenges the market faces as it attempts to push deeper into record territory. While investors have largely looked past the U.S.-Iran conflict, it remains a potential source of volatility through its impact on oil prices and broader risk sentiment. More importantly, elevated energy costs could begin to pressure margins as earnings season comes into focus, making guidance critical in determining whether current growth expectations can hold.

U.S. Treasuries retreated on Tuesday with shorter tenors extending their losses from Monday while the long bond reluctantly followed after holding its ground yesterday. The 2-year note yield settled up six basis points to 3.78%, and the 10-year note yield settled up four basis points to 4.29%.

BENCHMARK INDICES YEAR-TO-DATE

- Russell 2000: +11.4% YTD

- S&P Mid Cap 400: +10.4% YTD

- Nasdaq Composite: +4.4% YTD

- S&P 500: +3.2% YTD

- DJIA: +2.3% YTD

MARKET INTERNALS

- DOW closed lower at 49149 (-0.59%).

- Nasdaq closed lower at 24259 (-0.59%).

- S&P 500 closed lower at 7064 (-0.63%).

- Action came on lower than average volume for NYSE but not Nasdaq (NYSE 1,142 mln vs avg. of 1,390 mln; NASDAQ 9,393 mln vs avg. of 9,150 mln),

- Advancing/declining volume for NYSE (327 mln/805 mln) and Nasdaq (3860 mln/5457 mln).

- Decliners led advancers (NYSE 775/1987; NASDAQ 1324/3544)

- New 52-week highs outpacing new 52-week lows (NYSE 158/13, NASDAQ 312/79).

After-Hours Action

Main Stock market indexes closed around 0.6% lower on Tuesday as investors worried a US-Iran peace deal would not be reached before the ceasefire expires Wednesday. Concerns grew after Vice President JD Vance’s trip for Iran talks was paused due to Tehran’s lack of commitment. Still, after the closing bell, President Trump extended the US ceasefire with Iran, saying Tehran’s government was “seriously fractured.” He said the truce would remain in place until Iran’s leaders present a “unified proposal” to end the war. On Tuesday, UnitedHealth Group shares rose more than 8% after first-quarter results beat Wall Street expectations and the company raised its earnings outlook. Meanwhile, Amazon gained over 1% after agreeing to invest up to $25 billion in AI startup Anthropic.

After Hours Gainers:

Companies trading higher in after hours in reaction to earnings/guidance: MANH +9.1%, AXG +8.2%, MCRI +3.6%, PEGA +2.9%, ADC +2.7%, WAL +1.7%, TFIN +1.2%, UAL +1.1%, RRC +1%, EQT +0.6%, ISRG +0.5%, NLY +0.3%, EWBC +0.1%

Companies trading higher in after hours in reaction to news: GTLB +5.1% (deepens integration with Amazon Web Services), AMRZ +2% (shareholders approved all proposals), IMRX +2% (to present new survival data), OTIS +1.9% (increases dividend), ADBE +1.9% (authorizes new $25 bln share repurchase program), VICI +1.6% (new separate triple-net lease with an affiliate of Clairvest), ASRT +1.3% (provides update on Garda Therapeutics tender process), HBAN +1.1% (expands presence in Texas), TMQ +1.1% (commencement of permitting for high-grade Artic project in Alaska), LLY +0.6% (LLY to terminate license and collaboration agreement with RIGL), TOL +0.5% (to acquire substantially all the assets of Buffington Homes of Arkansas), META +0.5% (commences construction on $1+ bln data center in Oklahoma, according to Reuters), NOC +0.5% (files mixed securities shelf offering), BBOT +0.4% (presents preclinical data), JAZZ +0.3% (to present data at ASCO 2026), RVMD +0.1% (to present data for Daraxonrasib)

After Hours Losers:

Companies trading lower in after hours in reaction to earnings/guidance: SON -8.6%, CYH -8.1%, CALX -5% (also increases share repurchase authorization by $100 mln), DRVN -3.8%, COF -2.2% (also reports March card metrics), WFRD -2.2%, IBKR -1.8%, OZK -1.4%, CB -1%

Companies trading lower in after hours in reaction to news: TH -10.4% (announces launch of 7 mln share offering by selling shareholders), RIGL -4% (LLY to terminate license and collaboration agreement with RIGL), ASND -2.3% (has called $575 mln of convertible notes for redemption), KR -0.1% (files mixed securities shelf offering)

BONDS AND YIELDS

U.S. Treasuries retreated on Tuesday with shorter tenors extending their losses from Monday while the long bond reluctantly followed after holding its ground yesterday. The market faced some early pressure after a night that saw the release of solid February labor market figures from the U.K., which sent the 10-yr Gilt yield to 5.15%, its highest level in 28 years. Treasuries held their ground in immediate reaction to the March Retail Sales report (1.7%; Briefing.com consensus 1.3%), which beat expectations, largely thanks to higher gas prices. The early losses were extended in mid-morning trade as the market grew more concerned about the lack of updates from U.S.-Iran negotiations. The market learned in the late morning that Vice President Vance was still in Washington with just over 24 hours until tomorrow’s expiration of the ceasefire agreement. Today’s selling lifted yields on 10s and shorter tenors to levels from the middle of last week while relative strength in the long bond kept its yield near the midpoint of yesterday’s range. Crude oil climbed back above $90/bbl, pausing just below its settlement from Thursday. The U.S. Dollar Index rose 0.3% to 98.41, tagging its 200-day moving average (98.53) in the process.

Yields

- 2-yr: +6 bps to 3.78%

- 3-yr: +6 bps to 3.79%

- 5-yr: +6 bps to 3.91%

- 10-yr: +4 bps to 4.29%

- 30-yr: +2 bps to 4.90%

ROTW UPDATES

Equity indices in the Asia-Pacific region had a mostly higher showing on Tuesday.

- Japan’s Nikkei: +0.9%,

- Hong Kong’s Hang Seng: +0.5%,

- China’s Shanghai Composite: +0.1%,

- India’s Sensex: +1.0%,

- South Korea’s Kospi: +2.7%,

- Australia’s ASX All Ordinaries: UNCH.

In news:

- South Korea’s exports were up 49.4% through the first 20 days of April with chip exports jumping 182.5%.

- China Securities Journal noted that measures aimed at stabilizing the stock market have gained traction.

- Fitch expects China’s fiscal deficit to remain at 7.3% of GDP in 2026.

- New Zealand’s CPI remained above target for the second consecutive quarter in the reading for Q1.

In economic data:

- New Zealand’s Q1 CPI 0.9% qtr/qtr (expected 0.8%; last 0.6%); 3.1% yr/yr (expected 2.9%; last 3.1%). Q1 NZIER Business Confidence -4% (last 48%) and Q1 NZIER Capacity Utilization 91.2% (last 89.8%)

Major European indices trade with modest gains.

- STOXX Europe 600: +0.2%,

- Germany’s DAX: +0.3%,

- U.K.’s FTSE 100: -0.1%,

- France’s CAC 40: +0.2%,

- Italy’s FTSE MIB: +0.3%,

- Spain’s IBEX 35: +0.5%.

In news:

- European Central Bank policymaker Rehn said that there is no set rate path and that the current starting point is “reasonably balanced.”

- Meanwhile, ECB President Lagarde said that the central bank’s response will be determined by the duration of the energy shock.

- French Prime Minister Lecornu is seeking EUR4 bln in spending cuts.

- Germany’s ZEW institute noted that expectations are slipping into negative territory.

In economic data:

- Eurozone’s April ZEW Economic Sentiment -20.4 (expected -12.7; last -8.5)

- Germany’s April ZEW Economic Sentiment -17.2 (expected -6.7; last -0.5) and ZEW Current Conditions -73.7 (expected -70.0; last -62.9)

- U.K.’s February three-month employment change 25,000 (last 84,000). February Average Earnings Index + Bonus 3.8% yr/yr (expected 3.6%; last 4.1%). February Unemployment Rate 4.9%(expected 5.2%; last 5.2%) and March Claimant Count change 26,800 (expected 21,400; last 17,100)

- Spain’s February trade deficit EUR3.30 bln (last deficit of EUR4.00 bln)

- Swiss March trade surplus CHF3.177 bln (last surplus of CHF4.105 bln)

U.S. ECONOMIC UPDATES

- March Retail Sales 1.7% (Briefing.com consensus 1.3%); Prior was revised to 0.7% from 0.6%, March Retail Sales, ex-auto 1.9% (Briefing.com consensus 0.9%); Prior was revised to 0.7% from 0.5%

- The key takeaway from the report is that retail sales look great from a headline perspective, but higher gas prices and higher prices in general were the main drivers. Excluding gasoline sales, retail sales were up 0.6% month-over-month, which looks good, but remember retail sales are not adjusted for price changes. Accordingly, it becomes evident that the sales gains in March were driven more by higher prices than increased volume, which is a better indication of demand.

- February Business Inventories 0.4% (Briefing.com consensus 0.1%); Prior -0.1%

- March Pending Home Sales 1.5% (Briefing.com consensus 0.5%); Prior was revised to 2.5% from 1.8%

- Vice President JD Vance will leave today for Iran peace talks in Pakistan. Iranian officials privately say they will attend the talks as long as Mr. Vance is there, but they are refusing to confirm that publicly, according to NY Times

- The Senate will hold a confirmation hearing for Fed Chairman nominee Kevin Warsh this morning, according to CBS News

- Department of War says “Overnight, U.S. forces conducted a right-of-visit, maritime interdiction and boarding of the stateless sanctioned M/T Tifani without incident in the INDOPACOM area of responsibility.”

- White House Issues Memo related to Development, Manufacturing, and Deployment of Large-Scale Energy and Energy Related Infrastructure

- Department of Labor Secretary Lori Chavez-DeRemer to step down; Keith Sonderling to take over, according to White House Communications Director Steven Cheung

- Israel sees “non-existent” chances of U.S. deal with Iran, according to Al Monitor

- Vice President JD Vance’s flight to Pakistan has been put on hold after Iran failed to respond to U.S. negotiating positions, according to NY Times

- Iran’s leadership remains divided on whether to participate in peace talks, according to Axios

- Iranian Ambassador Amir Saeid Iravani says his government is seeing “some signs” that U.S. is ready to lift the blockade, according to AP News

- Vice President JD Vance could still leave this evening for Pakistan, but President Trump is also considering cancelling his trip all together because Iran is unwilling to give up nuclear enrichment, according to WSJ

US Crude Oil Inventories Post Surprise Draw

United States crude oil inventories fell by 4.40 million barrels in the week ended April 17th 2026, well above the 1.0 million barrel draw expected by markets and reversing a 6.10 million barrel increase in the previous week, according to the American Petroleum Institute. Gasoline inventories rose by 0.63 million barrels following a 3.97 million barrel decline in the previous period. Distillate stockpiles which include diesel and heating oil decreased by 3.40 million barrels following a 0.60 million barrel drop in the previous period.

US Pending Home Sales Rise Further

US pending home sales rose by 1.5% from the previous month in March of 2026, extending the upwardly revised 2.5% increase from February, and significantly outperforming the market expectation of a 0.1% increase. The increase was carried by a 4.4% increase in the Northeast region and a 3.8% jump in the South region, which offset the 2.6% drop in the West and 1.3% decrease in the Midwest. “Contract signings rose in March despite higher mortgage rates, pointing to pent-up housing demand,” said NAR Chief Economist Dr. Lawrence Yun. “A greater supply of inventory will help translate that demand into more home sales. Demand sensitivity to mortgage rates is greatest among first-time buyers, particularly younger buyers,” Yun said. “As a result, boosting supply and new-home construction should focus on smaller, more affordable homes.”

US Business Inventory Growth Hits Over 1-Year High

US business inventories rose by 0.4% month-over-month in February 2026, after a revised flat reading in January, slightly above the market consensus of a 0.3% increase. This marked the strongest gain since January 2025, driven by a sharp rebound in inventories at merchant wholesale inventories (0.8% vs -0.3%). Stocks also increased for retailers (0.2% vs 0.3%) and manufacturers (0.1% vs 0.1%). On a yearly basis, total business inventories went up by 1.3% in February.

US Retail Sales Rise by Most in a Year

US retail sales rose sharply by 1.7% in March 2026, surpassing market expectations of 1.4% and following an upwardly revised 0.7% increase in February. This marks the steepest growth since March 2025, driven largely by a record 15.5% surge in gasoline station receipts as fuel prices spiked amid the escalating conflict with Iran. Despite rising pump prices, consumer spending remained solid across nearly all categories, likely boosted by larger-than-usual tax refunds. Sales increased at motor vehicle and parts dealers (0.5%), furniture and home furnishing stores (2.2%), electronics and appliance stores (0.9%), building material and garden equipment suppliers (0.7%), food and beverage stores (0.7%), health and personal care stores (0.5%), general merchandise stores (1.0%), and nonstore retailers (1.0%). Receipts at restaurants and bars, the only service-sector category in the report, advanced 0.1%. Core retail sales, excluding volatile sectors, climbed 0.7%, exceeding forecasts of 0.2%.

US Weekly Job Growth Surges in Early April

US private employers added an average of 54,750 jobs per week in the four weeks ending April 4, 2026, according to the ADP Research Institute. This marks a significant acceleration from the upwardly revised 40,250 weekly jobs in the previous period and represents the fifth straight week of improving hiring activity. The latest figures also set a new record since weekly tracking began in September 2025.

COMMENTARY

I am still sick. Will write more soon.

Stay Hedged – My Penguin Friends

(Excerpts from briefing.com, tradingeconomics.com, financialscents.com, factset.com, finviz.com, marketwatch.com, etrade.com, yahoo.com, tigerbrokers.com, tradingview.com, tradingcentral.com, theedgemalaysia.com, sectorspdrs.com, Investopedia.com, and CNBC.com)