DMA of 2026 APRIL 08 WEDNESDAY AMC.

The stock market rallied today as a two-week ceasefire agreement between the U.S. and Iran culminated in a sharp retreat in oil prices and a meaningful improvement in sentiment across equities.

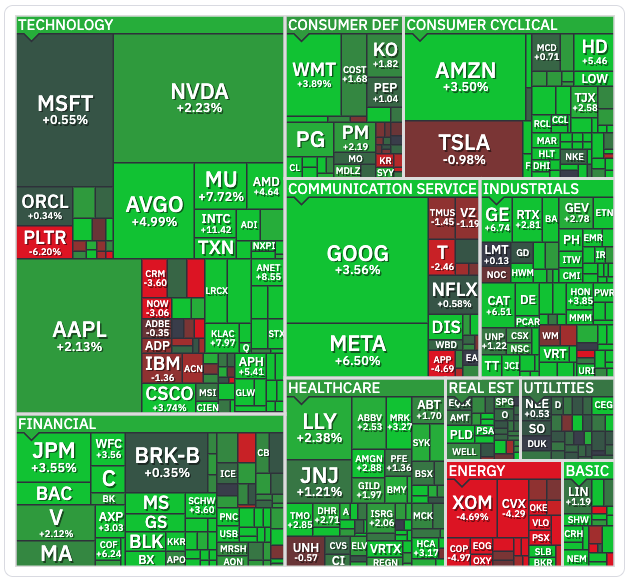

The S&P 500 (+2.3%), Nasdaq Composite (+2.8%), and DJIA (+2.9%) posted broad gains that saw the major averages reclaim their 200-day moving averages, with the S&P 500 closing just above its 50-day moving average (6,765) as well. The Russell 2000 (+3.0%) and S&P Mid Cap 400 (+2.8%) notched similar gains as the broader market displayed a clear risk-on disposition today.

Bloomberg reported that the U.S. and Iran are set to hold talks to seek a more permanent end to the war soon, marking a much more conciliatory tone in comparison to yesterday’s rhetoric. However, the situation remains delicate, with Israeli strikes against targets in Lebanon drawing condemnation from Iran and threats to abandon the agreement.

Still, today’s action marked a definitive step towards a resolution. Tanker traffic has yet to pick up through the Strait of Hormuz, but crude oil futures still settled today’s session $18.45 lower (-16.4%) at $94.40 per barrel.

The energy sector (-3.7%) faced a sharp retreat as a result, but the ten other S&P 500 sectors finished with gains of 1.0% or wider.

The industrials sector (+3.8%) led the advance, supported by strong gains across airline names such as United Airlines (UAL 96.30, +7.01, +7.85%) amid the retreat in oil prices. Delta Air Lines (DAL 68.08, +2.46, +3.75%) beat earnings expectations, and the company emphasized that it is not seeing any slowdown in summer travel demand despite higher ticket prices and macro headwinds.

Similarly, cruise lines such as Carnival (CCL 28.03, +2.83, +11.23%) posted double-digit gains today as oil slid, helping the consumer discretionary sector (+2.8%) finish near the top of the leaderboard as well.

Elsewhere in the sector, homebuilders also captured solid gains amid hopes that an easing of the Iran conflict may bring mortgage rates back down.

Amazon (AMZN 221.25, +7.48, +3.50%) provided solid mega-cap leadership, though Tesla (TSLA 343.23, -3.42, -0.99%) continues its recent slide, finishing as the only “magnificent seven” stock without a gain today.

Meanwhile, Meta Platforms (META 612.42, +37.37, +6.50%) captured a monster gain following the unveiling of Muse Spark, its first step toward personal superintelligence with multimodal, multi-agent AI.

Chipmakers were also a point of strength as today’s bullish session reignited momentum in the AI trade. The PHLX Semiconductor Index finished 6.3% higher, helping the broader information technology sector (+2.8%) shake off relative weakness across its software components.

Today’s data was limited, though the March FOMC minutes showed inflation remains above target, with higher oil prices adding near-term pressure. While officials still expect a gradual return to 2%, geopolitical risks could delay progress.

Investors will turn their attention to tomorrow’s February PCE Price Index (Briefing.com consensus 0.4%), the Fed’s preferred measure of inflation. While today’s temporary ceasefire sparked a broad relief rally, focus now shifts to the path toward a more durable resolution—particularly the reopening of the Strait of Hormuz, which would help alleviate pressure on oil prices and the resulting inflation concerns.

U.S. Treasuries finished Wednesday with solid gains across the curve, though intraday action saw a steady retreat from opening highs. The 2-year note yield settled down four basis points to 3.79%, and the 10-year note yield settled down five basis points to 4.29%.

BENCHMARK INDICES YEAR-TO-DATE

- S&P Mid Cap 400: +6.6% YTD

- Russell 2000: +5.6% YTD

- DJIA: -0.3% YTD

- S&P 500: -0.9% YTD

- Nasdaq Composite: -2.6% YTD

MARKET INTERNALS

- DOW closed higher at 47910 (+2.85%).

- Nasdaq closed higher at 22635 (+2.80%).

- S&P 500 closed higher at 6783 (+2.51%).

- Action came on higher than average volume (NYSE 1,498 mln vs avg. of 1,432 mln; NASDAQ 10,580 mln vs avg. of 9,115 mln),

- Advancing/declining volume for NYSE (1122 mln/366 mln) and Nasdaq (8255 mln/2314 mln).

- Advancers led decliners (NYSE 2338/447; NASDAQ 3662/1182)

- New 52-week highs outpacing new 52-week lows (NYSE 107/21, NASDAQ 209/78).

After-Hours Action

US stocks closed sharply higher on Wednesday as investors remained optimistic that two week ceasfire between Iran and US will last. The White House said the US would engage in direct talks with Iran, even as ongoing Middle East fighting, including Israeli strikes in Lebanon and Iran strikes on Gulf states risked undermining the ceasefire. The Dow ended the seesion more than 1,300 points higher, or 2.85%, marking the best day since April 2025. The S&P 500 jumped 2.5% and the Nasdaq surged 2.80%. Oil prices were sharply lower and yields held their recent drop, rekindling risk sentiment despite warnings of stagflation in the latest FOMC minutes. Speculative AI stocks were higher with Nvidia, Meta, Tesla, AMD, and Micron surging between 4% and 10%. Airlines also jumped on the improved outlook of jet fuel supply, and Delta soared 6% after posting earnings.

After Hours Gainers:

Companies trading higher in after hours in reaction to earnings/guidance: STAA +19.7% (guides Q1 revenue well above consensus), RELL +8.4%, RGP +5.1%

Companies trading higher in after hours in reaction to news: RCEL +7.3% (enters into long term agreement with BARDA valued up to $25.5 mln), MGNX +3.8% (FDA removes partial clinical hold on study of lorigerlimab), MRAM +2.6% (MRAM and MCHP announce manufacturing agreement to boost production capacity), DT +2.3% (to acquire Bindplane), NUAI +1.4% (commences stock offering), FBRX +1.1% (commences stock offering), BETR +1.1% (execs purchase shares on open market), XWIN +0.9% (announces key milestone in its AI strategy), ICFI +0.5% (awarded position on new $800 mln digital modernization BPA), AGX +0.3% (increases share repurchase authorization to $200 mln), DAL +0.3% (expects 2026 capital spend of about $5.5 bln; discusses fuel outlook), LHX +0.3% (co-development deal with Xoople for satellite constellation), NDAQ +0.1% (reports March monthly volumes)

After Hours Losers:

Companies trading lower in after hours in reaction to earnings/guidance: APLD -5.8%, STZ -1%, INFQ -0.7%, PSMT -0.1%

Companies trading lower in after hours in reaction to news: HURA -5% (files prospectus supplement relating to sales agreement; may offer up to $50 mln of common stock), AEHR -4.4% (enters equity distribution agreement, may offer up to $60 mln of common stock), ASRT -1.8% (to be acquired by Garda Therapeutics for $18/sh), PSFE -1.7% (MoonPay is now powering crypto payments inside its platform), INTC -0.9% (repurchased 49% interest from Apollo-managed funds in joint venture related to Intel’s Fab 34 in Ireland), COST -0.5% (reports March comps), CAT -0.3% (CFO to retire, names new CFO), FDX -0.3% (reaches tentative agreement with Air Line Pilots Assn)

BONDS AND YIELDS

U.S. Treasuries finished Wednesday with solid gains across the curve, though intraday action saw a steady retreat from opening highs. Treasuries opened the day with big gains that sent yields to three-week lows as global investor sentiment improved after President Trump agreed to a two-week ceasefire with Iran. The lasting power of the agreement remains in question, but the market took a more optimistic view of the conflict for the time being. The strong start in Treasuries took place alongside big gains in other sovereign debt and a sharp drop in the price of oil, which reached an intraday low of $91/bbl, down nearly $22/bbl from yesterday’s closing level. Treasuries inched above their starting levels during the first couple minutes of action, but then reversed, spending the rest of the day in a slow retreat from highs. The market stayed near midday lows in immediate reaction to a weak $39 bln 10-yr note reopening but slipped to fresh lows during the last hour of trade, ending near the midpoint of today’s range with yields near last week’s lows. The final dip was a continuation of the steady pullback, but it also followed the release of March FOMC Minutes, which showed growing interest among policymakers in using two-sided language when discussing the expected rate path. Many participants observed that higher inflation could call for rate hikes while most officials were concerned that an extended war could result in job cuts that would warrant cuts to the fed funds rate range. Crude oil settled below $95/bbl while the U.S. Dollar Index fell 0.8% to 99.11.

Yields

- 2-yr: -4 bps to 3.79%

- 3-yr: -5 bps to 3.81%

- 5-yr: -6 bps to 3.92%

- 10-yr: -5 bps to 4.29%

- 30-yr: -3 bps to 4.89%

CURRENCIES

The dollar Index remained below 99 on Wednesday, hovering near its lowest level in about a month, as news of a two-week ceasefire between the United States and Iran, which triggered a sharp drop in oil prices, eased investor concerns about an inflationary spiral and boosted expectations that the Fed could cut interest rates this year. At the start of the week, markets had priced in no chance of a rate cut, having previously anticipated more than two reductions before the conflict escalated. Meanwhile, minutes from the FOMC’s March meeting showed policymakers were concerned that Middle East hostilities could lead to sustained inflation requiring further rate hikes, although they still expected one rate cut this year. Investors now await the release of US March CPI data on Friday for additional clues on price pressures linked to the ongoing conflict.

Currencies

- EUR/USD: +0.5% to 1.1652

- GBP/USD: +0.7% to 1.3390

- USD/CNH: -0.3% to 6.8360

- USD/JPY: -0.5% to 158.69

Sterling Rallies as US-Iran Truce Eases Risk

The British pound rose 1% to $1.34, nearing its strongest level since late February, after the US and Iran secured a last-minute two-week ceasefire ahead of President Donald Trump’s deadline. The deal, pausing the US-Israel offensive in return for Iran reopening the Strait of Hormuz, has sparked cautious optimism for a short-term easing of Middle East tensions, though deeper conflicts persist. The truce has bolstered risk appetite, with plunging oil and gas prices prompting investors to downgrade Bank of England rate hike expectations. Markets now price in just one rate increase for 2026, down from two before the agreement.

Euro Surges as US-Iran Ceasefire Sparks Risk Rally

The euro climbed to $1.17, its highest level since late February, after the US and Iran struck a two-week ceasefire just hours before President Donald Trump’s deadline expired. The agreement, halting the US-Israel military campaign in exchange for Iran reopening the Strait of Hormuz, has fueled hopes of a temporary de-escalation in the Middle East, though broader tensions remain unresolved. The ceasefire has triggered a shift toward risk assets, with the sharp drop in oil and European gas prices prompting investors to scale back expectations for ECB rate hikes. Markets now anticipate only two rate increases this year, down from three before the truce.

COMMODITIES

Brent crude futures jumped nearly 2% toward $97 per barrel and WTI crude futures jumped more than 2% toward $97 per barrel on Thursday, recovering part of the prior session’s losses as renewed Israeli strikes on Lebanon raised doubts about the durability of a fragile Middle East ceasefire, while the Strait of Hormuz remains largely obstructed. Iranian media reported that oil tanker traffic through the strait had been suspended following the attacks, amid disputes between Tehran and the American-Israeli side over whether the truce extends to Lebanon. A senior Iranian official also stated that three provisions of the ceasefire agreement have already been breached. Meanwhile, US Vice President JD Vance said there are indications the strait may begin reopening as he leads a US delegation to Islamabad for direct talks with Iran this weekend. The near shutdown of Hormuz, which handles about 20% of global crude and gas flows, has triggered the most severe disruption in oil markets.

The spread between Brent and WTI is currently at $0.04

Commodities

- Crude Oil -18.45 @ 94.40

- Nat Gas -0.15 @ 2.72

- Gold +90.70 @ 4776.70

- Silver +3.41 @ 75.40

- Copper +0.22 @ 5.78

Silver Prices Cut Some Gains

Silver prices pared earlier gains but remained up about 1% at $73.9 per ounce on Wednesday, after rising sharply as the US and Iran agreed to a temporary two-week ceasefire, which includes the reopening of the Strait of Hormuz and a suspension of US military strikes. In response, oil prices plunged, the dollar weakened, and bond yields declined, all of which supported demand for the white metal. However, some investors moved to take profits as risk appetite returned to global equity markets. At the same time, caution persisted amid reports of localized airstrikes in the region, underscoring the fragility of the Pakistan-brokered truce. Meanwhile, minutes from the FOMC’s March meeting showed policymakers were concerned that Middle East hostilities could lead to sustained inflation requiring further rate hikes, although they still expected one rate cut this year. Since the Iran conflict began on February 28, silver has fallen by nearly 20%.

Gold Pares Most Gains

Gold prices pared most of the earlier gains but remained in positive territory on Wednesday, holding above $4,700 per ounce, as traders continued to assess developments in the Middle East and their implications for the economic and monetary outlook. The US and Iran agreed to a temporary two-week ceasefire, including the reopening of the Strait of Hormuz and a suspension of US military strikes. In response, oil prices plunged, the dollar weakened, and bond yields declined, all of which supported demand for bullion. However, some investors moved to take profits as risk appetite returned to global equity markets. At the same time, caution persisted amid reports of localized airstrikes in the region, underscoring the fragility of the Pakistan-brokered truce. Meanwhile, minutes from the FOMC’s March meeting showed policymakers were concerned that Middle East hostilities could lead to sustained inflation requiring further rate hikes, although they still expected one rate cut this year.

Orange Juice Hits 9-week High

Orange Juice increased to 206.00 USd/Lbs, the highest since February 2026. Over the past 4 weeks, Orange Juice gained 11.24%, and in the last 12 months, it decreased 22.54%.

Nickel Prices Rise on Supply Control

Nickel futures traded around $17,300 per tonne, climbing from recent levels, as Indonesia’s quota cut supported investor confidence. The country has signaled continued production discipline for its 2026 quota, with RKAB approvals indicating output in the range of roughly 190–200 million tons, reinforcing market sentiment despite ongoing oversupply. Prices have stabilized in the $17,000–$17,400 range as markets adjust to the tighter quotas. However, gains remain capped as global inventories are still elevated and the overall market is projected to run a surplus in 2026. Demand has stayed subdued, with stainless steel production ample and overall manufacturing activity weak, while battery sector adoption trends have yet to drive a sharp rise in demand this month. In addition, policy support emerged in April, with Western Australia offering interest-free loans to help nickel miners resume operations and ramp up production.

ROTW UPDATES

Equity indices in the Asia-Pacific region ended the midweek session on a broadly higher note, encouraged by President Trump delaying the deadline for strikes on Iran’s infrastructure due to progress in talks.

- Japan’s Nikkei: +5.4%,

- Hong Kong’s Hang Seng: +3.1%,

- China’s Shanghai Composite: +2.7%,

- India’s Sensex: +4.0%,

- South Korea’s Kospi: +6.9%,

- Australia’s ASX All Ordinaries: +2.7%.

In news:

- Japan’s cash earnings for February grew at their fastest pace since September while real cash earnings increased for the second month in a row.

- Japan’s Finance Minister Katayama said that it is still uncertain if an extra budget will be needed.

- The Reserve Bank of India left its policy rate at 5.25%, as expected, while the Reserve Bank of New Zealand left its official cash rate at 2.25%, which was also expected, though RBNZ policymakers discussed a rate hike.

In economic data:

- Japan’s February Average Cash Earnings 3.3% yr/yr (expected 2.7%; last 2.5%) and Overall Wage Income 3.3% yr/yr (expected 2.7%; last 2.5%). February Current Account surplus JPY2.71 trln (expected surplus of JPY2.40 trln; last surplus of JPY3.13 trln). March Economy Watchers Current Index 42.2 (expected 48.0; last 48.9)

- South Korea’s February Current Account surplus $23.19 bln (last surplus of $13.26 bln)

- Hong Kong’s March Manufacturing PMI 49.3 (last 53.3)

Major European indices trade with solid gains alongside a drop in energy prices after President Trump agreed to a two-week ceasefire with Iran.

- STOXX Europe 600: +4.2%,

- Germany’s DAX: +5.1%,

- U.K.’s FTSE 100: +3.0%,

- France’s CAC 40: +4.8%,

- Italy’s FTSE MIB: +4.2%,

- Spain’s IBEX 35: +4.3%.

In news:

- Sovereign debt also trades broadly higher with Germany’s 10-yr yield falling 15 basis points to a three-week low of 2.93% while Italy’s 10-yr yield is down 23 basis points to 3.69%, which also marks a three-week low.

- Germany reported weak Factory Orders growth for February (0.9%; expected 3.0%), making for just a small rebound from a sharp drop in January (-11.1%).

In economic data:

- Eurozone’s February Retail Sales -0.2% m/m, as expected (last 0.0%); 1.7% yr/yr (expected 1.6%; last 2.1%). February PPI -0.7% m/m (expected -0.6%: last 0.8%); -3.0% yr/yr, as expected (last -2.0%)

- Germany’s February Factory Orders 0.9% m/m (expected 3.0%; last -11.1%)

- U.K.’s March Halifax House Price Index -0.5% m/m (expected 0.2%; last 0.3%); 0.8% yr/yr (expected 1.5%; last 1.2%)

- France’s February trade deficit EUR5.8 bln (expected deficit of EUR2.4 bln; last deficit of EUR2.0 bln)

- Swiss March Unemployment Rate 3.0%, as expected (last 3.0%)

U.S. ECONOMIC UPDATES

- Weekly MBA Mortgage Applications Index -0.8%; Prior -10.4%

- U.S., Iran, and Israel agree to two week ceasefire; Iran says safe passage through the Strait of Hormuz is possible for two weeks with “due consideration of technical limitations”; first round of talks to end war start Friday; S&P futures rise 2.7%; WTI crude oil plunges 16%

- President Trump says Iran went through a “very productive regime change”; says will discuss sanctions relief with Iran; says many of the 15 points have already been been agreed to

- CNN reporter Alayna Treene says “Iranian President Masoud Pezeshkian has confirmed that his country will take part in ceasefire talks in Islamabad on Friday, according to a statement from Pakistani Prime Minister Shehbaz Sharif’s office on Wednesday”

- Iran wants fees for ships passing through Strait of Hormuz during the two week ceasefire, according to FT

- A maritime security company urged caution because Iran said it would reopen the Strait of Hormuz under military control, according to WSJ

- Iranian Supreme Leader Mojtaba Khamenei instructed his negotiators to move toward a deal two days ago, according to Axios

- Vice JD Vance says the Iran ceasefire is a “fragile truce.”, CNBC

- The Trump administration plans to cut the Iran funding request to $80-100 billion from $200 billion prior, according to Washington Post

- Treasury wants to meet with state insurance commissioners about private credit risk, according to WSJ

- Republican Clay Fuller wins a special election in Georgia, which will expand the Republican House majority by one member, according to NY Times

- Iran will charge ships $1 per barrel of oil for traveling through Strait of Hormuz; money will be paid in cryptocurrency; empty ships will travel for free, according to FT

- Halt of military strikes mostly holding after ceasefire agreement, according to Washington Post

- Iran says it will withdraw from ceasefire deal if Israeli attacks on Lebanon continue (Lebanon is home of the Iranian proxy Hezbollah), according to Bloomberg

- U.S. and Iran agree to hold discussions to end war even as Israeli strikes on Lebanon could upend the ceasefire deal, according to Bloomberg

- Israel’s security cabinet will meet tonight to discuss ceasefire, according to WSJ

- President Trump denounces “fraudsters” sending unauthorized Iran negotiation letters; says meaningful points will be discussed “behind closed doors”

- CMS issues guidance to implement new limits on Federal Medicaid and CHIP funding for certain noncitizens

- Chris Phelan is a frontrunner to be the next Chair of the Council of Economic Advisers, according to Politico

Fed Signals Openness to Rate Hikes

Some Fed officials favoured a two-sided framing of future rate decisions, highlighting that additional increases could be warranted if inflation persists above target levels, minutes from the last FOMC meeting in March showed. The vast majority of participants judged that upside risks to inflation and downside risks to employment were elevated, and the majority of participants noted that these risks had increased with developments in the Middle East. A prolonged conflict in the Middle East would likely lead to more persistent increases in energy prices and these higher input costs would be more likely to pass through to core inflation. The Fed left the federal funds rate steady at the 3.5%–3.75% target range for a 2nd consecutive meeting in March 2026, in line with expectations. However, policymakers still signaled one reduction in the fed funds rate this year and another in 2027, though the timing remains unclear.

US Crude Oil Inventories Rise More than Expected

US crude inventories rose by 3.1 million barrels to 464.7 million barrels in the week ended April 3, compared with market expectations for a 701,000-barrel rise. Crude stocks at the Cushing, Oklahoma, delivery hub rose by 24,000 barrels in the week. Refinery crude runs fell by 129,000 barrels per day, while utilization rates fell by 0.1 percentage points to 92% in the week. US gasoline stocks fell by 1.6 million barrels in the week to 239.3 million barrels, compared with expectations for a 1.4 million-barrel draw. Distillate stockpiles, which include diesel and heating oil, fell by 3.1 million barrels in the week to 114.7 million barrels, versus expectations for a 1.5 million-barrel drop. Net US crude imports fell last week by 758,000 barrels per day, EIA said.US

Mortgage Rates Dip Amid Middle East Uncertainty

The average US 30-year fixed mortgage rate for conforming loans of $806,500 or less fell to 6.51% for the week ending April 3, 2026, down from a seven-month high of 6.57% the prior week, the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey showed on Wednesday. This marks the first decline in over a month, driven by a 10+bps drop in Treasury yields as investors grew wary of the Middle East conflict’s economic impact. The war has rattled global markets, fueling stagflation fears and reducing expectations that the Fed will raise rates this year to curb energy-driven inflation. Despite the rate dip, mortgage activity weakened: total applications fell 0.8%, the fourth consecutive weekly decline, including prior drops exceeding 10%. Refinancing activity led the drop, down 2.8%, while purchase applications inched up 1.1%.

US Mortgage Applications Fall for 4th Week

Mortgage applications in the US eased by 0.8% from the previous week on the period ending April 3rd, extending the cumulative 28.5% plunge from the three previous weeks, according to data compiled by the Mortgage Bankers Association. The recent pullback was extended despite the respite for benchmark mortgage rates, which pulled back from the seven-month high last week. Long-dated Treasury yields retreated from recent peaks in the period as markets considered the growth side of stagflation concerns, easing bets that the Fed could return to hikes this year to contain energy-induced price growth. Still, credit sentiment for households remained muted on the large levels of uncertainty. Applications for a contract to refinance a mortgage, which are more sensitive to short-term changes in interest rates, fell by 3%. In turn, applications for a mortgage to buy a new home inched higher by 1% but fell 7% from the previous year, the first annual decline since January 2025.

EARNINGS SEASON AND GUIDANCE

- Aehr Test Systems (AEHR) beats by $0.02, slightly misses on revs; Reaffirms FY26 guidance

- Better Home & Finance (BETR) reports Q1 2026 preliminary Funded Loan Volume of $1.64 bln, exceeding prior guidance of $1.40-1.55 bln

- Delta Air Lines (DAL) beats by $0.06, beats on revs; guides Q2 EPS below consensus

- Endeavour Silver (EXK) produces 1,875,375 Oz silver and 11,740 Oz gold, for a total of 3.3 million silver equivalent oz in Q1 2026

- FedEx Freight (FDX) will host its inaugural Investor Day today ahead of its planned spinoff from FedEx Corporation; Separation remains on track for completion on June 1, 2026

- Greenbrier (GBX) misses by $0.35, misses on revs; guides FY26 EPS below consensus, revs below consensus

- Jefferies (JEF) discloses gross mark-to-market loss of $42.8 mln associated with Market Financial Solutions during Q1

- Levi Strauss (LEVI) beats by $0.05, beats on revs; raises FY26 EPS and revneue guidance; guides Q2 EPS and revenue in-line

- OR Royalties (OR) sees Q1 revs below consensus

- Phoenix Education Partners (PXED) beats by $0.24, reports revs in-line; reaffirms FY26 revs guidance; authorizes $50 mln share repurchase program

- Regeneron Pharma (REGN) expects Q1 to include IPR&D charge of $102 mln and negatively impact income per share by about $0.81

- RPM Inc (RPM) beats by $0.22, beats on revs; reaffirms outlook

- SEALSQ Corp (LAES) reports Q1 2026 key financial and operational metrics; reaffirms FY 2026 revenue guidance; reaffirms that the QS7001 certification process is progressing

- Shell (SHEL) first quarter 2026 update note

- United Micro (UMC) reports March sales increased 4.89% yr/yr to ~NT$20.83 bln

2026 APR 09

Pre-Market: NEOG SMPL

After-Hours: WDFC

THE WEEK AHEAD

WEEK 15: MONDAY TO FRIDAY, APRIL 06 to APRIL 10

According to the PTSD*, Week 15 has FIVE trading days and is the SECOND trading week in April 2026. The next Market Holiday is on MONDAY MAY25. Seasonally, Week 15 has a Bullish outlook, leading to an even greener week 16 and 17. April is the last of the “6 months of bullishness” on the SPX.

We also need to keep in mind that with the current POTUS, seasonals can easily go out of whack.

*PTSD – Penguin Trader Seasonal Data.

BENCHMARK INDICES (21-YEAR AVERAGE)

The Stock Trader’s Almanac’s stats for the Benchmark Indices for 2026 APRIL 09 of Week 15 over a 21-year average are:

- Dow Jones (DJIA): 66.7%

- S&P 500 (SPX): 61.9%

- NASDAQ (COMP): 667%

- *Russells 2000 (RUT): 61.9%

*The RUT is not listed in the STA; several penguins with a slide ruler calculated the 21-year average.

BENCHMARK INDEX ETFs

The Penguin Trader Seasonal Data (PTSD) stats for the Benchmark Index ETFs for 2026 APRIL 09 of Week 15 over a 15-year average are:

- DIA – (15yr Avg): 66.7%

- SPY – (15yr Avg): 60.0%

- QQQ – (15yr Avg): 46.7%

- RUT – (15yr Avg): 53.3%

ECONOMIC DAY AHEAD

For USA’s upcoming economic calendar features:

- 8:30 ET: Weekly Initial Claims (Briefing.com consensus 215,000; prior 202,000), Continuing Claims (prior 1.841 mln), February Personal Income (Briefing.com consensus 0.5%; prior 0.4%), Personal Spending (Briefing.com consensus 0.6%; prior 0.4%), PCE Prices (Briefing.com consensus 0.4%; prior 0.3%), Core PCE Prices (Briefing.com consensus 0.3%; prior 0.4%), Q4 GDP — third estimate (Briefing.com consensus 0.7%; prior 0.7%), and Q4 GDP Deflator — third estimate (Briefing.com consensus 3.8%; prior 3.8%)

- 10:00 ET: February Wholesale Inventories (Briefing.com consensus -0.2%; prior NA)

- 10:30 ET: Weekly natural gas inventories (prior +36 bcf)

ANALYSIS

A penguin will be volunteered for this post soon, or if incentivised with enough cheese.

COMMENTARY

While it does look like a buying frenzy, the volumes are not showing. I would suggest tight stops and careful planning with a solid exit strategy for the bullish penguins.

On the home front, my IC is in the red. This is expected with the sudden spike upwards. I am still well within my safe zone; for now.

Stay Hedged – My Penguin Friends

(Excerpts from briefing.com, tradingeconomics.com, financialscents.com, factset.com, finviz.com, marketwatch.com, etrade.com, yahoo.com, tigerbrokers.com, tradingview.com, tradingcentral.com, theedgemalaysia.com, sectorspdrs.com, Investopedia.com, and CNBC.com)