DMA of 2026 APRIL 07 TUESDAY AMC.

20260407 – 0800SGT

US Futures Rally on Two-Week Ceasefire

US stock futures rallied on Wednesday after President Donald Trump delayed his threat to strike Iranian civilian infrastructure by two weeks, announcing what he called a “double-sided ceasefire”. Dow, S&P 500 and Nasdaq 100 futures were all up by more than 2%. Trump also said the US had received a 10-point proposal from Iran that he described as a “workable basis for negotiations,” with the two-week window allowing the potential agreement to be finalized and implemented. Additionally, Iran has agreed to reopen the Strait of Hormuz for two weeks provided all attacks are halted, adding that transit would need to be coordinated with Iran’s Armed Forces, while Israel has also reportedly agreed to the ceasefire. In regular trading on Tuesday, the Dow fell 0.18%, while the S&P 500 and Nasdaq Composite gained 0.08% and 0.1%, respectively.

Stocks had a choppy session, with the major averages facing several intraday swings amid conflicting reports regarding the state of ceasefire negotiations between the U.S. and Iran. The S&P 500 (+0.1%), Nasdaq Composite (+0.1%), and DJIA (-0.2%) opened to losses of roughly 1.0% as President Trump’s 8:00 p.m. ET deadline loomed, with the president threatening a “whole civilization will die tonight” if a deal is not struck.

The major averages fluctuated throughout the session amid conflicting reports of where negotiations stood or if communications between the U.S. and Iran were even open.

In the final hour of the session, Pakistani Prime Minister Shehbaz Sharif requested that President Trump extend the deadline for two weeks and that Iran open the Strait of Hormuz for a corresponding period of two weeks. Pakistan is a key mediator in the negotiations, and White House Press Secretary Karoline Leavitt said that the President has been made aware of the proposal, and a response will come.

Crude oil futures settled today’s session $0.60 higher (+0.5%) at $112.85 per barrel, which was well off session highs, but retreated even further following the Pakistani peace proposal.

The late session rally saw five S&P 500 sectors finish with gains after participation was notably weaker for most of the session.

The communication services sector (+1.0%) captured the widest gain, with Paramount Skydance (PSKY 10.90, +1.05, +10.66%) finishing as the best-performing S&P 500 component after the company confirmed commitments from Saudi-wealth funds for its takeover of Warner Bros. Discovery (WBD 27.37, -0.04, -0.15%).

Alphabet (GOOG 303.93, +6.27, +2.11%) was a mega-cap standout after announcing a long-term partnership with Broadcom (AVGO 333.97, +19.54, +6.21%), in which Broadcom will work to develop and supply custom Tensor Processing Units (TPUs) to Google.

Strength across chipmaker names helped the information technology sector (+0.4%) notch a higher finish after holding an early loss that exceeded 1.0%. Apple (AAPL 253.50, -5.36, -2.07%) was a laggard today after Nikkei Asia reported that its foldable iPhone will likely be delayed due to engineering hurdles.

Elsewhere, managed care names such as UnitedHealth (UNH 307.73, +26.37, +9.37%) and Humana (HUM 197.15, +14.50, +7.94%) rallied after the Centers for Medicare & Medicaid Services released its CY27 Medicare Advantage (MA) and Part D Rate Announcement, which came in meaningfully better than expected and eased concerns about ongoing margin pressure.

The health care sector (+0.2%) notched a modest gain, while the utilities sector (+0.3%) finished similarly, and the energy sector (+0.8%) outperformed.

Meanwhile, the consumer staples (-1.8%) and consumer discretionary (-0.9%) sectors were today’s worst performers, with particular weakness across specialty stores and homebuilders.

Similar to the S&P 500 and Nasdaq Composite, the Russell 2000 (+0.2%) and S&P Mid Cap 400 (+0.1%) eked out a gain as the broader market rallied in the final hour of the session.

Today’s action underscores that oil prices are continuing to drive the stock market, with the major averages whipsawing intraday amid conflicting reports on U.S.–Iran ceasefire negotiations ahead of tonight’s 8:00 p.m. ET deadline. The approaching deadline adds urgency to the headlines, keeping volatility elevated. Until there is more clarity on the outcome, markets are likely to remain sensitive to every development in the U.S.–Iran talks.

U.S. Treasuries had a mixed showing on Tuesday, as shorter tenors recovered from a lower start while longer tenors could not stay out of the red. The bounce off morning lows found some midday resistance, but a strong $58 bln 3-year note auction gave the complex an afternoon boost that helped 5s and shorter tenors finish in the green. The 2-year note yield settled down two basis points to 3.83%, and the 10-year note yield settled up one basis point to 4.34%.

BENCHMARK INDICES YEAR-TO-DATE

- S&P Mid Cap 400: +3.7% YTD

- Russell 2000: +2.5% YTD

- DJIA: -3.1% YTD

- S&P 500: -3.3% YTD

- Nasdaq Composite: -5.3% YTD

MARKET INTERNALS

- DOW closed lower at 46584 (-0.18%).

- Nasdaq closed higher at 22017 (+0.10%).

- S&P 500 closed higher at 6616 (+0.08%).

- Action came on higher than average volume for Nasdaq but not NYSE (NYSE 1,112 mln vs avg. of 1,432 mln; NASDAQ 10,998 mln vs avg. of 9,059 mln),

- Advancing/declining volume for NYSE (454 mln/646 mln) and Nasdaq (7626 mln/3304 mln).

- Decliners led advancers (NYSE 1308/1435; NASDAQ 2216/2588)

- Mixed new 52-week highs and new 52-week lows (NYSE 45/45, NASDAQ 77/148).

After-Hours Action

US stock futures rallied on Wednesday after President Donald Trump delayed his threat to strike Iranian civilian infrastructure by two weeks, announcing what he called a “double-sided ceasefire”. Dow, S&P 500 and Nasdaq 100 futures were all up by more than 2%. Trump also said the US had received a 10-point proposal from Iran that he described as a “workable basis for negotiations,” with the two-week window allowing the potential agreement to be finalized and implemented. Additionally, Iran has agreed to reopen the Strait of Hormuz for two weeks provided all attacks are halted, adding that transit would need to be coordinated with Iran’s Armed Forces, while Israel has also reportedly agreed to the ceasefire. In regular trading on Tuesday, the Dow fell 0.18%, while the S&P 500 and Nasdaq Composite gained 0.08% and 0.1%, respectively.

After Hours Gainers:

Companies trading higher in after hours in reaction to earnings/guidance: PXED +7.9% (also authorizes new $50 mln share repurchase program), LEVI +6.5% (also CFGO to retire)

Companies trading higher in after hours in reaction to news: OSCR +6% (CEO bought 1 mln shares worth ~$11.9 mln), DBD +3.8% (to join S&P SmallCap 600), ASR +1.9% (March traffic), NTNX +1.7% (authorizes $750 mln increase to its share repurchase program), KDK +1.3% (expands autonomous trucking beyond the Sunbelt), RGTI +1.1% (general availability of Cepheus-1-108Q), VALE +0.4% (accelerates Oman maintenance outages, according to Bloomberg), SMCI +0.3% (provides update on investigation), APP +0.1% (names new CTO and new Chairperson), VET +0.1% (reports Q1 production; advances portfolio repositioning)

After Hours Losers:

Companies trading lower in after hours in reaction to earnings/guidance: GBX -5.6%, KRUS -4.1% (also CFO to step down), AEHR -2.5%

Companies trading lower in after hours in reaction to news: TBN -14% (files mixed securities shelf offering), LXU -1.7% (settlement related to construction of ammonia plant), LAND -1.4% (files for $1 bln mixed securities shelf offering), STNG -1.2% ($300 mln convertible note offering and concurrent stock repurchase), GD -1% (awarded $450 mln agreement from US Marine Corps), EQ -1% (stock offering by selling shareholders), SLB -0.7% (collaboration between PETRONAS Suriname E&P), INSM -0.6% (update on Phase 2b CEDAR study; brensocatib did not meet its primary or secondary efficacy endpoints), GRAL -0.1% (collaboration with Epic)

BONDS AND YIELDS

U.S. Treasuries had a mixed showing on Tuesday, as shorter tenors recovered from a lower start while longer tenors could not stay out of the red. The trading day started with losses in most tenors and weakness in other sovereign debt as investors remained focused on the price of oil, which climbed back above $115/bbl in morning trade, making a brief push toward its March high (119.48). The market attempted to put together an early bounce after the Durable Orders report for February (-1.4%; Briefing.com consensus 0.5%) showed an unexpected headline decrease that masked solid growth in capital goods spending. Treasuries faced renewed selling in mid-morning action, sliding alongside a weak open on Wall Street. Both markets reached lows around 11:00 ET, battling back from those levels over the next few hours while oil retreated from its highest level of the day. The moves followed some speculation that an off-ramp could appear ahead of tonight’s 20:00 ET deadline that President Trump imposed on talks with Iran. The bounce off morning lows found some midday resistance, but a strong $58 bln 3-yr note auction gave the complex an afternoon boost that helped 5s and shorter tenors finish in the green. Crude oil approached $113/bbl while the U.S. Dollar Index fell 0.2% to 99.83.

Yields

- 2-yr: -2 bps to 3.83%

- 3-yr: -1 bp to 3.86%

- 5-yr: -1 bp to 3.98%

- 10-yr: +1 bp to 4.34%

- 30-yr: +3 bps to 4.92%

CURRENCIES

The dollar index hovered around the 100 mark on Tuesday as traders weighed escalating tensions in the Middle East alongside the approaching deadline set by President Trump for Iran to reach an agreement. President Trump warned that, unless his conditions including the reopening of the Strait of Hormuz are met by 8 p.m. Eastern Time, the US could target key Iranian infrastructure. He later intensified his rhetoric, stating that “a whole civilization will die tonight” unless Iran’s leadership agrees to a deal that includes reopening the Strait. Meanwhile, reports indicate that Iran has halted negotiation efforts with the US. On the data front, consumer inflation expectations rose in March, while the logistics sector experienced a notable increase in transportation costs. Looking ahead, the release of US March CPI data on Friday is expected to provide further insight into price pressures potentially linked to the ongoing conflict.

Currencies

- EUR/USD: +0.3% to 1.1576

- GBP/USD: +0.2% to 1.3258

- USD/CNH: -0.2% to 6.8629

- USD/JPY: +0.1% to 159.84

Chinese Yuan Hits 5-week High

The Chinese Yuan touched 6.86 against the USD, the highest since February 2026. Over the past 4 weeks, US Dollar Chinese Yuan lost 0.4%, and in the last 12 months, it decreased 7.6%.

Sterling Stalls Amid Iran Deadline and Energy Surge

The British pound showed little movement against the dollar, hovering just above $1.32, as markets adopted a cautious “wait-and-see” stance ahead of Trump’s Iran deadline. US President Trump escalated warnings, demanding Iran reopen the Strait of Hormuz by today, or face “devastating” US strikes, including attacks on bridges and power plants, despite potential Geneva Convention violations. Meanwhile, Iran’s continued blockade of LNG tankers has worsened global fuel shortages, pushing energy prices higher and reinforcing expectations of tighter monetary policy. Markets now firmly price in two Bank of England rate hikes this year.

Euro Steady as Trump’s Iran Threats Fuel Market Uncertainty

The euro remained stable against the dollar on Tuesday, hovering around $1.154, as European investors returned from the Easter break to assess the escalating Middle East conflict. US President Trump intensified threats against Iran, warning that the Strait of Hormuz must reopen by today’s deadline, or face devastating US strikes, including targeting bridges and power plants. Meanwhile, Iran has continued to block liquefied natural gas (LNG) tankers from passing through the strait, deepening a global fuel shortage. The resulting surge in energy prices has reinforced expectations of tighter monetary policy, with markets now pricing in three European Central Bank interest rate hikes this year. On Monday, ECB Governing Council member Pierre Wunsch told the Wall Street Journal that the bank may raise rates multiple times, starting as early as this month, if the Middle East-driven energy crisis lingers.

COMMODITIES

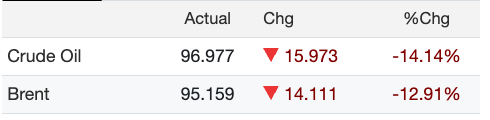

Brent crude futures plunged more than 15% toward $90 per barrel and WTI crude futures plunged more than 15% to below $95 per barrel on Wednesday after President Donald Trump delayed his threat to attack Iranian civilian infrastructure by two weeks in what he described as a “double-sided ceasefire,” contingent on Iran reopening the Strait of Hormuz. Trump also said the US had received a 10-point proposal from Iran that he described as a “workable basis for negotiations,” with the two-week window allowing the potential agreement to be finalized and implemented. Additionally, Iran has agreed to reopen the Strait of Hormuz for two weeks provided all attacks are halted, adding that transit would need to be coordinated with Iran’s Armed Forces, while Israel has also reportedly assented to the temporary ceasefire. The near-closure of the vital waterway, through which about 20% of global oil flows, has roiled energy markets and heightened risks of rising inflation and a global economic slowdown.

The spread between Brent and WTI is currently at $1.82

Commodities

- Crude Oil +0.60 @ 112.85

- Nat Gas +0.06 @ 2.87

- Gold +2.80 @ 4686.00

- Silver -0.91 @ 71.99

- Copper -0.04 @ 5.56

Heating Oil Tumbles 17%

Heating oil futures tumbled more than 17% to below $3.70 per gallon on Wednesday, hitting a four-week low, after Iran agreed to temporarily reopen the Strait of Hormuz under a two-week ceasefire with the US and Israel. Iranian Foreign Minister Abbas Araghchi said safe transit through the strait would be coordinated with the country’s armed forces, accounting for technical constraints. Earlier, President Donald Trump noted that the ceasefire depends on Iran reopening the waterway, which would allow an agreement to be finalized. Israel has also reportedly agreed to pause strikes while negotiations continue, and the first round of US-Iran talks is set to take place in Islamabad on Friday. The announcement came less than two hours before Trump’s deadline for Iran to reopen the vital waterway or face military strikes targeting its power plants and bridges.

Silver Rallies as Trump Delays Strikes for 2 Weeks

Silver jumped more than 4% to above $76 per ounce on Wednesday, hitting a three-week high after President Donald Trump delayed his planned strikes on Iranian civilian infrastructure by two weeks to finalize talks on a potential resolution to the war. Trump also said the US had received a 10-point proposal from Iran that he described as a “workable basis for negotiations,” with the two-week window allowing the potential agreement to be finalized and implemented. Additionally, Iran has agreed to reopen the Strait of Hormuz for two weeks provided all attacks are halted, adding that transit would need to be coordinated with Iran’s Armed Forces, while Israel has also reportedly assented to the temporary ceasefire. Silver has tumbled as much as 37% peak-to-trough since the conflict began, as a surge in energy prices fueled inflation concerns and reinforced a hawkish shift in central bank outlooks.

Gold Jumps as Trump Delays Strikes Anew

Gold jumped more than 2% to above $4,800 per ounce on Wednesday, extending recent gains after President Donald Trump delayed his planned strikes on Iranian civilian infrastructure by two weeks to finalize talks on a potential resolution to the war. Trump also said the US had received a 10-point proposal from Iran that he described as a “workable basis for negotiations,” with the two-week window allowing the potential agreement to be finalized and implemented. Additionally, Iran has agreed to reopen the Strait of Hormuz for two weeks provided all attacks are halted, adding that transit would need to be coordinated with Iran’s Armed Forces, while Israel has also reportedly assented to the temporary ceasefire. Gold has tumbled as much as 25% peak-to-trough since the conflict began, as a surge in energy prices fueled inflation concerns and reinforced a hawkish shift in central bank outlooks.

ROTW UPDATES

Equity indices in the Asia-Pacific region ended Tuesday on a higher note while Hong Kong’s Hang Seng remained closed for Easter.

- Japan’s Nikkei: UNCH,

- Hong Kong’s Hang Seng: HOLIDAY,

- China’s Shanghai Composite: +0.3%,

- India’s Sensex: +0.7%,

- South Korea’s Kospi: +0.8%,

- Australia’s ASX All Ordinaries: +1.7%.

In news:

- Japan sold 30-yr JGBs to weak demand despite a downsized auction.

- South Korea’s policy chief said that South Korean chip fabricators have secured a four-month supply of helium.

- Samsung Electronics reported record results for Q1.

- The Reserve Bank of New Zealand and Reserve Bank of India will opine tomorrow, but policy changes are not expected.

In economic data:

- China’s March FX Reserves $3.342 trln (expected $3.400 trln; last $3.428 trln)

- Japan’s February Leading Index 112.4, as expected (last 112.1) and Coincident Indicator -1.6% m/m (last 3.4%). February Household Spending 1.5% m/m (expected 2.6%; last -2.5%); -1.8% yr/yr (expected -0.8%; last -1.0%)

- Australia’s March Services PMI 46.3 (expected 46.6; last 52.8). March MI Inflation Gauge 1.3% m/m (last -0.2%) and March ANZ Job Advertisements -3.1% m/m (last 3.2%)

Major European indices trade in mixed fashion after a four-day Easter weekend.

- STOXX Europe 600: -0.2%,

- Germany’s DAX: -0.2%,

- U.K.’s FTSE 100: -0.1%,

- France’s CAC 40: +0.53%,

- Italy’s FTSE MIB: +0.3%,

- Spain’s IBEX 35: +0.2%.

In news:

- European Central Bank policymaker Wunsch said that a lasting crisis could invite a series of rate hikes, and that he is open to a hike later this month while policymaker Radev said that it is too early to tell if an April rate hike is needed.

- Final March Services PMI readings from the region’s major economies were mostly better than expected, though Italy (48.8) and France (48.8) reported contractionary readings.

In economic data:

- Eurozone’s March Services PMI 50.2 (expected 50.1; last 51.9). April Sentix Investor Confidence -19.2 (expected -7.5; last -3.1)

- Germany’s March Services PMI 50.9 (expected 51.2; last 53.5)

- U.K.’s March Services PMI 50.5 (expected 51.2; last 53.9)

- France’s March Services PMI 48.8 (expected 48.3; last 49.6)

- Italy’s March Services PMI 48.8 (expected 51.0; last 52.3)

- Spain’s March Services PMI 53.3 (expected 50.7; last 51.9)

- Swiss March Foreign Reserves $721.2 bln (last $710.1 bln)

U.S. ECONOMIC UPDATES

- Durable goods orders decreased 1.4% month-over-month in February (Briefing.com consensus: 0.5%) following a downwardly revised 0.5% decline (from 0.0%) in January. Excluding transportation, durable goods orders increased 0.8% (Briefing.com consensus: 0.5%) following a downwardly revised 0.3% increase (from 0.4%) in January.

- The key takeaway from the report is that the weakness in February was concentrated largely in transportation and capital goods orders. Otherwise, order activity was decent, highlighted by a 0.6% increase in new orders for nondefense capital goods, excluding aircraft—a proxy for business spending.

- Consumer credit increased by $9.5 billion in February (Briefing.com consensus $7.0 billion) after increasing by a revised $7.7 billion (from $8.1 billion) in January. Nonrevolving credit increased by $8.8 billion while revolving credit increased by $700 million.

US Crude Oil Inventories Increase for 4th Week

United States crude oil inventories jumped by 3.72 million barrels in the week ended April 3rd 2026 as stocks continued to climb for a fourth straight week following a significant 10.263 million barrel increase in the previous week. Gasoline inventories fell by 3.97 million barrels following a 3.209 million barrel decline in the previous period. Distillate stockpiles which include diesel and heating oil decreased by 599,000 barrels following a 1.04 million barrel drop in the previous period.

US Consumer Credit Misses Expectations in February

Total US consumer credit rose by $9.48 billion in February 2026, following a downwardly revised $7.67 billion gain in January and below market expectations of a $10 billion increase. It is equivalent to an increase of about 2.2% at an annual rate. Revolving credit increased by $0.71 billion in February, after increasing $2.57 billion in January. Nonrevolving credit, which includes auto and student loans, rose $8.79 billion in February, following a $5.10 billion gain in the previous month.

US Durable Goods Orders Drop for 3rd Month

New orders for US-manufactured durable goods fell by 1.4% from the previous month to $315.5 billion in February of 2026, extending the revised 0.5% drop in the previous month. It was the third straight decline in orders, contrasting with leading indicators for the sector that reflected stronger demand for goods producers. Orders sank for transportation equipment (-5.4% to $106.1 billion) due to a -28.6% plunge in nondefense aircraft and parts (to $19.2 billion). Excluding transportation equipment, new orders inched higher by 0.8%, with support from primary metals (2.2% to $28.6 billion) and machinery (1.5% to $41.1 billion).

US Private-Sector Hiring Surges in March

US private employers added an average of 26,000 jobs per week in the four weeks ending March 21, 2026, according to the ADP Research Institute, a significant jump from the 15,250 weekly jobs created in the previous period. This marks the third consecutive week of hiring growth, with job creation reaching its highest level since weekly records began in September 2025. The data signals a robust rebound in the labor market.

US Logistics Growth Highest Since 2022 on Soaring Prices

The Logistics Manager’s Index in the US increased to 65.7 in March 2026, the highest since May 2022, from 61.5 in February, driven by continued expansion in the freight market. Transportation Prices skyrocketed (+12.7 to 89.4, a new high level since March of 2022), at least partially attributable to the start of the Iran conflict that has limited available oil supplies. This stands in contrast with the continued contraction of Transportation Capacity (-1.8 to 39.2), at least partially due to the reduction of fleet capacity of the last few years. The 50.2-point gap between these two metrics is the highest positive inversion since November 2021. Meanwhile, Inventory Levels expanded slightly faster (+1.0 to 54.8) and Inventory Costs also moved higher (+8.4 to 76.2, the highest since August 2025). Also, Warehousing Capacity contracted (-4 to 46) and Warehousing Utilization expansion slowed (-0.6 to 59.8) while Warehousing Prices increased (+4.8 to 67.4).

US Inflation Expectations Rise Sharply

Median year-ahead inflation expectations measured by the New York Fed rose to 3.4% in March of 2026 from 3% in the previous month, the highest so far this year. Consumer expectations for gasoline (9.4% vs 4.1% in February) price growth surged to the highest level since March of 2022 as the outbreak of war in the Middle East lifted benchmark energy prices. Inflation expectations were also higher for food (6% vs 5.3%) and rent (7.1% vs 5.9%). Meanwhile, inflation expectations for the three-year-ahead horizon edged up by 0.1 percentage point to 3.1% and were unchanged at 3% at the five-year-ahead horizon in March. Elsewhere, spending and household income growth expectations remained largely unchanged. Consumers were more pessimistic about their future household financial situations.

US Used-Vehicle Prices Hit 2023 Highs

Wholesale used-vehicle prices in the US climbed 1.4% month-over-month in March 2026, marking the fifth straight month of increases and pushing the Manheim Used Vehicle Value Index to 215.3, its highest level since summer 2023. Prices also surged 6.2% year-over-year. Jeremy Robb, Cox Automotive’s chief economist, attributed the strength to strong consumer demand fueled by higher tax refunds and tight inventory levels, despite initial concerns over the Middle East conflict’s impact. Cox noted that sales conversion rates remained above normal in Q1, signaling robust dealer demand. Electric vehicle (EV) prices at wholesale are also rising as off-lease EV maturities increase, driving EV weighting in the Manheim index to a record 3.9% in March. Dealers appear to be stocking up on used EVs, anticipating higher demand as gas prices surpass $4.00 per gallon.

US Economic Sentiment Falls to Near 2-Year Low

The RealClearMarkets/TIPP Economic Optimism Index fell sharply to 42.8 in April 2026, the lowest level since June 2024, down from 47.5 in March and below expectations of 48.1, as concerns over the Middle East war and rising gasoline prices weighed on sentiment. The index has now remained below the neutral 50 mark for eight straight months, signaling persistent pessimism. The Six Month Economic Outlook dropped 10.5% to 38.5, reflecting growing doubts about the economy’s near-term prospects. The Personal Financial Outlook also weakened, slipping 7.6% to 50.2. Meanwhile, confidence in Federal Economic Policies deteriorated significantly, with the gauge falling to 39.8 from 45.1, highlighting rising skepticism over the government’s ability to manage economic challenges amid heightened uncertainty.

- Negotiations are not confident an Iran deal will be reached ahead of President Trump’s 8pm eastern time deadline where he has threatened to target bridges and energy infrastructure, according to WSJ

- srael targeting dozens of Iranian infrastructure sites; U.S. strike hit railway bridge, according to Bloomberg

- Iran rejects U.S. ceasefire terms; Explosions were heard on Kharg Island, but the source of the explosions is not clear, according to Bloomberg

- Axios reporter Barak Ravid says “The U.S. military conducted strikes on military targets on Kharg island, U.S. official says”

- President Trump is considering seizing control of Iran’s oil to gain leverage against China, according to Bloomberg

- DHS Secretary Markwayne Mullin says his agency could take action against international airports in sanctuary cities if those cities do not cooperate with immigration authorities, according to NY Post

- CMS finalizes 2027 Medicare Advantage and Part D payment policies

- UK car sales rise highest level since 2019, according to Bloomberg

- Iran cuts off direct communications with the U.S., according to WSJ

- U.S.-Iran talks show small progress ahead of President Trump’s 8 p.m. deadline, according to Axios

- Pakistan Prime Minister Shehbaz Sharif requests President Trump extend deadline for two weeks and Iran open Strait of Hormuz for a corresponding period of two weeks (Note: Pakistan is a key mediator in talks)

- Israel wants longer war with Iran, but President Trump is pushing for deal, according to Politico

EARNINGS SEASON AND GUIDANCE

- Academy Sports + Outdoors (ASO) guides Q1 revenue above consensus ahead of its Analyst Day today

- Aris Mining (ARIS) reports Q1 2026 production and strong revenue growth

- Hon Hai Precision (HNHPF) reports March sales increased 45.6% yr/yr to NT$803.7 bln

- LGI Homes (LGIH) reports Q1 closings and community count

- Mesoblast (MESO) reports $30.3 mln quarterly sales for Ryoncil

- Pembina (PPL) Business Update Highlights Strategic Focus and Growth Outlook

- Phillips 66 (PSX) provides guidance on certain items impacting first-quarter 2026 results

- Samsung (SSNLF) reports preliminary Q1 results

2026 APR 08

Pre-Market: DAL RPM

After-Hours: APLD STZ PSMT

THE WEEK AHEAD

WEEK 15: MONDAY TO FRIDAY, APRIL 06 to APRIL 10

According to the PTSD*, Week 15 has FIVE trading days and is the SECOND trading week in April 2026. The next Market Holiday is on MONDAY MAY25. Seasonally, Week 15 has a Bullish outlook, leading to an even greener week 16 and 17. April is the last of the “6 months of bullishness” on the SPX.

We also need to keep in mind that with the current POTUS, seasonals can easily go out of whack.

*PTSD – Penguin Trader Seasonal Data.

BENCHMARK INDICES (21-YEAR AVERAGE)

The Stock Trader’s Almanac’s stats for the Benchmark Indices for 2026 APRIL 08 of Week 15 over a 21-year average are:

- Dow Jones (DJIA): 47.6%

- S&P 500 (SPX): 47.6%

- NASDAQ (COMP): 33.3%

- *Russells 2000 (RUT): 57.1%

*The RUT is not listed in the STA; several penguins with a slide ruler calculated the 21-year average.

BENCHMARK INDEX ETFs

The Penguin Trader Seasonal Data (PTSD) stats for the Benchmark Index ETFs for 2026 APRIL 08 of Week 15 over a 15-year average are:

- DIA – (15yr Avg): 73.3%

- SPY – (15yr Avg): 60.0%

- QQQ – (15yr Avg): 66.7%

- RUT – (15yr Avg): 80.0%

Make of you what you will of the seasonal numbers. I believe that the News currently has diminished accuracy.

ECONOMIC DAY AHEAD

For USA’s upcoming economic calendar features:

- 7:00 ET: Weekly MBA Mortgage Index (prior -10.4%)

- 10:30 ET: Weekly crude oil inventories (prior +5.45 mln)

- 14:00 ET: March FOMC Minutes

ANALYSIS

A penguin will be volunteered for this post soon, or if incentivised with enough cheese.

COMMENTARY

The very scary, naughty, big bads were averted or delayed in the Middle East. Again. As expected. I believe that if Main Street can predict these patterns with too much accuracy, these patterns will change.

On the home front, my ICs are still flapping away, this time with one of the wings bleeding in the negative. But it is alright. I was selling volatility, and the crush just happened. Just wait for SPX to consolidate some.

Stay Hedged – My Penguin Friends

(Excerpts from briefing.com, tradingeconomics.com, financialscents.com, factset.com, finviz.com, marketwatch.com, etrade.com, yahoo.com, tigerbrokers.com, tradingview.com, tradingcentral.com, theedgemalaysia.com, sectorspdrs.com, Investopedia.com, and CNBC.com)