DMA of 2026 MARCH 31 TUESDAY AMC.

Stocks rallied today as leaders from both the U.S. and Iran signaled a willingness to end the ongoing conflict that has sent energy prices soaring and stocks lower over the past month.

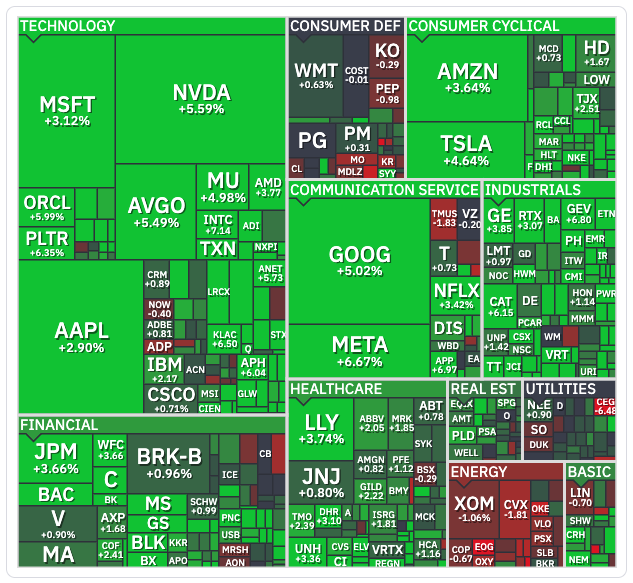

In the final session of March, the S&P 500 (+2.9%), Nasdaq Composite (+3.8%), and DJIA (+2.5%) took back a considerable chunk of previous weakness, ultimately ending March with losses ranging from 4.8% to 5.5%. The month-to-date figure is notable given that the U.S. and Israel launched joint strikes against Iran on February 28, which was a Saturday, meaning the war in Iran has been at the forefront of the market’s focus since the first opening bell of March.

Equity futures pointed to a higher opening this morning after The Wall Street Journal reported that President Trump told aides he is willing to end U.S. military operations against Iran even if the Strait of Hormuz remains closed, as reopening it could extend the conflict beyond the 4- to 6-week timeline.

Out of the gate, stocks climbed in broad fashion, with solid mega-cap leadership supporting growth at the index level, unlike yesterday’s session. Gains across the major averages doubled shortly after midday following a CNBC report that Iranian state media said the country’s president spoke by phone with the European Council. Iran is reportedly “prepared to end the war” with guarantees against further attacks, a call that has been confirmed by the European Council President.

In the wake of the reports, oil prices retreated modestly after a flattish morning, ultimately settling $1.77 lower (-1.7%) at $101.15 per barrel.

The energy sector (-1.1%) was a laggard as a result, while the utilities (-0.1%) and consumer staples (flat) sectors also went overlooked as the geopolitical optimism translated into a risk-on rally.

Tech and other growth-oriented sectors posted some of the strongest gains, with communication services (+4.4%) leading the sector leaderboard. Meta Platforms (META 572.13, +35.75, +6.67%) and Alphabet (GOOG 286.90, +13.76, +5.04%) extended their recent rebounds from last week’s lows that followed news that the companies were found liable in a social media addiction trial.

The information technology sector (+4.2%) posted a similar gain as NVIDIA (NVDA 174.44, +9.28, +5.62%) and other semiconductor stocks rebounded nicely after a weak showing yesterday. The PHLX Semiconductor Index (+6.2%) reclaimed all of yesterday’s losses and then some, and onsemi (ON 61.92, +6.26, +11.25%) was one of the best-performing S&P 500 components.

Other outperformers included airlines and cruise lines such as United Airlines (UAL 92.07, +6.86, +8.05%) and Carnival (CCL 25.88, +1.92, +8.01%) as oil prices stabilized today, while stocks tied to bitcoin and gold also mounted solid gains.

Outside of the S&P 500, the Russell 2000 (+3.4%) and S&P Mid Cap 400 (+2.8%) finished with gains similar to those across the major averages.

All told, today’s session marked a meaningful uptick in sentiment as talks of a ceasefire in the war in Iran gained traction, with Tehran now signaling a willingness to end the conflict under certain conditions—a notable shift from just days ago, when it had rejected ceasefire proposals outright. The S&P 500 captured its widest single-day gain since last May, a much-needed relief rally after several weeks of downward momentum. However, the situation in Iran has proven to be delicate, and oil remains above the $100 per barrel mark, highlighting that a definitive end to the energy shock is not yet a certainty.

The major averages will enter the first session of the second quarter pinned below their respective 200-day moving averages, though today’s rally moved them significantly closer to the key technical level.

U.S. Treasuries ended March on a higher note, continuing Friday’s rebound off 2026 lows. The 2-year note yield settled down three basis points to 3.80% (+42 bps in March; +32 bps in Q1), and the 10-year note yield settled down three basis points to 4.31% (+35 bps in March; +14 bps in Q1).

BENCHMARK INDICES YEAR-TO-DATE

- S&P Mid Cap 400: +2.2% YTD

- Russell 2000: +0.6% YTD

- DJIA: -3.6% YTD

- S&P 500: -4.6% YTD

- Nasdaq Composite: -7.1% YTD

MARKET INTERNALS

- DOW closed higher at 46341 (+2.49%).

- Nasdaq closed higher at 21590 (+3.83%).

- S&P 500 closed higher at 6528 (+2.91%).

- Action came on higher than average volume (NYSE 1,744 mln vs avg. of 1,434 mln; NASDAQ 10,747 mln vs avg. of 9,086 mln),

- Advancing/declining volume for NYSE (1359 mln/364 mln) and Nasdaq (9109 mln/1596 mln).

- Advancers led decliners (NYSE 2148/626; NASDAQ 3924/953)

- New 52-week lows outpacing new 52-week highs (NYSE 56/126, NASDAQ 63/181).

After-Hours Action

U.S. equity futures edged up on Wednesday, extending momentum from Wall Street’s strong rally the previous day after the White House said President Trump will deliver an address later today on Iran. On Tuesday, Trump dismissed the need for a negotiated settlement to end the war, suggesting the U.S. could simply declare victory and halt hostilities. On the data front, US house prices rose 0.1% mom in January, with annual gains remaining subdued. Tech heavyweights led gains, with all members of the “Magnificent Seven” closing comfortably higher after a mixed performance on Monday. Meta surged 6.7% following a 2% rise at the start of the week, while Marvell Technology soared nearly 13% to pace the Nasdaq after unveiling a strategic partnership and USD 2 billion investment from Nvidia. Shares of the world’s most valuable company also advanced 5.6%, reinforcing optimism across the sector.

After Hours Gainers:

Companies trading higher in after hours in reaction to earnings/guidance: NCNO +19% (also authorizes $100 mln accelerated share repurchase program), OMER +7.5%, PLAY +5.4%, RILY +4.9%, PVH +1.8%, FBRX +0.9%

Companies trading higher in after hours in reaction to news: HHH +1.9% (reschedules shareholder meeting), FRPH +1.6% (to delay 10-K filing), DRS +0.8% (awarded a $533 mln Navy contract), AREC +0.8% (to delay 10-K filing), RYN +0.3% (will maintain the Rayonier name), VRTX +0.2% (completes submission to FDA of its rolling BLA for povetacicept)

After Hours Losers:

Companies trading lower in after hours in reaction to earnings/guidance: RH -16.9%, NKE -8.8%, POET -5.5%, ASTL -0.1%

Companies trading lower in after hours in reaction to news: ORIC -22.9% (reports Phase 3 data), INGM -2.2% (earns Microsoft Frontier Distributor designation), ACNT -2.1% (files for $100 mln mixed securities shelf offering), GLSI -1.7% (to delay 10-K filing), TMC -1.5% (files mixed securities shelf offering), ASPI -1.4% (to delay 10-K filing), FROG -0.9% (Platform is now available in the Cursor marketplace), AIR -0.9% (awarded a $305 mln Navy contract), RGTI -0.5% (announces Novera QPU sale), T -0.4% (commits up to $2 bln to modernize emergency cellular network, according to WSJ), INFQ -0.3% (stock offering; also stock offering by selling shareholders), SPGI -0.2% (launches new datasets), LMT -0.1% (awarded a $1.35 bln modification to previously awarded Navy contract)

BONDS AND YIELDS

U.S. Treasuries ended March on a higher note, continuing Friday’s rebound off 2026 lows. The Tuesday advance was paced by shorter tenors while the long end resisted, ending with just a slim gain. Treasuries opened with gains across the curve after a night that featured a torrent of month-end data from major economies. However, surprises were limited despite the barrage. China’s official Manufacturing (50.4) and Non-Manufacturing (50.1) PMI readings returned to expansion in March while economic data from Europe showed weak February Consumer Spending in France (-1.4% m/m; expected -0.3%) and cooler than expected flash March CPI from the eurozone (2.5% yr/yr; expected 2.6%). More notably, the market was focused and encouraged by President Trump’s comments that he is considering ending the Iran war without reopening the Strait of Hormuz. Later in the day, it was reported that Iran’s president signaled willingness to end the war if his country receives guarantees against additional attacks. That midday revelation prompted a jump to fresh highs in Treasuries and equities while oil gave back its gain, though it still ended the pit session above $100/bbl, jumping $34, or 50.8%, for the month. As for Treasuries, even with today’s gains, they recorded big losses for the month with the 2-yr yield jumping 42 basis points while the 10-yr yield increased by 35 basis points as rate cut expectations plummeted. The U.S. Dollar Index fell 0.6% to 99.92, narrowing its March advance to 2.3%.

Yields

- 2-yr: -3 bps to 3.80% (+42 bps in March; +32 bps in Q1)

- 3-yr: -4 bps to 3.82% (+44 bps in March; +28 bps in Q1)

- 5-yr: -3 bps to 3.95% (+44 bps in March; +22 bps in Q1)

- 10-yr: -3 bps to 4.31% (+35 bps in March; +14 bps in Q1)

- 30-yr: -1 bp to 4.89% (+26 bps in March; +4 bps in Q1)

CURRENCIES

The dollar index hovered around 99.8 on the first trading day of April, having risen 2.3% in March, supported by safe-haven demand amid lingering uncertainty over the trajectory of the Middle East conflict. While President Donald Trump suggested that the war could end within two to three weeks, traders remain cautious as more US troops are being deployed to the region and the Strait of Hormuz remains largely closed. The dollar was further supported by diminishing expectations of Federal Reserve rate cuts this year, as the conflict drove oil prices sharply higher, stoking inflation concerns. Meanwhile, Fed Chair Jerome Powell appeared to reassure markets, saying that long-term US inflation expectations remain grounded.

Currencies

- EUR/USD: +0.7% to 1.1541

- GBP/USD: +0.4% to 1.3225

- USD/CNH: -0.4% to 6.8899

- USD/JPY: -0.5% to 158.96

Offshore Yuan Steady Amid Peace Hopes

The offshore yuan stabilized around 6.88 per dollar on Wednesday, following significant gains in the previous session as optimism over a potential near-term resolution to the Middle East conflict dented demand for the greenback. US President Trump said American forces would end operations in Iran within two to three weeks, adding that Iran was “begging to make a deal” but that any agreement was “irrelevant” to Washington’s timeline. Iranian President Masoud Pezeshkian earlier said Tehran had the “necessary will” to end the conflict, provided safeguards prevent renewed hostilities. The yuan gained further support as BOC Hong Kong works with regulators to upgrade digital wallets, following China’s move to allow interest on the currency, a step that could boost offshore adoption. Meanwhile, a private survey showed the manufacturing PMI fell to 50.8 in March 2026, from 52.1 in February. In contrast, official data indicated the manufacturing PMI rebounded to a one-year high of 50.4.

Australian Dollar Rebounds from 2-Month Low

The Australian dollar rose to around $0.692, rebounding from a two-month low, supported by hopes for de-escalation of Middle East tensions. Global risk sentiment improved after Trump said the US could end its military attacks on Iran within two to three weeks and is set to address the nation later in the day, fueling speculation of a potential wind-down in the conflict. However, uncertainty persisted as reports suggested the US may deploy additional naval forces to the region, while concerns over the Strait of Hormuz kept oil prices supported amid fears of prolonged supply risks. The inflation impact of higher energy costs continued to cloud the outlook, with analysts warning it could keep prices elevated for longer and increase pressure on interest rates in Australia. The Reserve Bank, which raised rates to 4.10% in March, remains in focus, with markets pricing roughly a 65% chance of another hike at its May meeting, though expectations for the peak rate have eased slightly.

Japanese Yen Holds Gains

The Japanese yen held its gains around 158 per dollar on Wednesday, as market optimism grew over a potential de-escalation of tensions in the Middle East. Investors were encouraged by remarks from US President Donald Trump, who indicated that American forces would conclude operations in Iran “very soon,” suggesting a timeline of two to three weeks. On the Iranian side, President Masoud Pezeshkian expressed a willingness to end hostilities, provided guarantees are given that the conflict will not reignite. Domestically, Japan’s economic indicators underscored resilience despite the geopolitical uncertainty. The Bank of Japan’s sentiment index for large manufacturers rose to 17 in the first quarter of 2026, reaching its highest level since the fourth quarter of 2021, suggesting that business confidence remains robust. Meanwhile, the Manufacturing PMI was revised slightly up to 51.6 in March from a preliminary estimate of 51.4, but remained below February’s near four-year peak of 53.

South Korean Won Remains Under Pressure

The South Korean won hovered around 1,510 per dollar, remaining close to its weakest levels since 2009, as global risks and persistent capital outflows continued to weigh on the currency. Crude oil prices stayed elevated near $100 per barrel amid ongoing Middle East tensions, keeping imported inflation risks prominent. Additional downside pressure came from sustained capital outflows, with heavy net selling by foreign investors, amplifying demand for the greenback and weighing on the currency. Meanwhile, US President Donald Trump signaled that military operations in Iran could conclude within weeks. While this lifted market sentiment and eased some oil-driven inflation concerns, the currency’s recovery was limited by structural headwinds. The Bank of Korea has signaled readiness to intervene if volatility intensifies, helping to contain further losses. The won is likely to trade in a narrow range in the near term.

Rupee Slips Amid Outflows, High Oil Prices

The Indian rupee slipped to around 93.5 per dollar, pausing losses after stabilizing briefly as persistent geopolitical tensions and elevated oil prices continued to weigh on the currency. Although hopes have emerged that the conflict may end soon following statements from Donald Trump, lingering uncertainties are keeping investors cautious. March saw global funds withdraw around $12 billion from Indian equities, the steepest monthly outflow on record. Brent crude, up 44% since February, could climb further if the Strait of Hormuz remains effectively closed, adding to currency pressures. Analysts warn that if the conflict in Iran persists, the rupee could weaken to 100 per dollar or beyond, despite recent measures by the Reserve Bank of India to curb its roughly 10% decline over the past year. Market positioning remains bearish, with options pricing indicating roughly a 13% chance of the rupee reaching 100 by June and a 41% probability by year-end.

COMMODITIES

Brent crude oil futures rose above $105 per barrel and WTI crude oil futures rose toward $103 per barrel on Wednesday, recouping losses from the previous session and extending their record monthly jump, as markets weighed President Trump’s remarks amid fresh attacks in the Persian Gulf. Trump told reporters that US forces could withdraw from Iran within two to three weeks and suggested a deal with Tehran might be possible but was not required to end the conflict. However, markets remained cautious as additional US troops arrived in the region, and Tehran said no formal peace talks were underway but signaled willingness to end the war if its conditions are met. All eyes are now on Trump’s nationwide address on the Iran conflict later today. Meanwhile, Iranian drones struck fuel tanks at Kuwait International Airport, triggering a large fire and damaging the tanks, adding to recent attacks on energy infrastructure. Elsewhere, API data showed US crude inventories surged by 10.263 million barrels last week.

The spread between Brent and WTI is currently at $1.70

Commodities

- Crude Oil -1.77 @ 101.15

- Nat Gas -0.01 @ 2.88

- Gold +122.50 @ 4679.50

- Silver +4.24 @ 74.87

- Copper +0.11 @ 5.61

Iron Ore Rises as Stimulus Bets Rise

Iron ore futures rose to around CNY 815 per ton, rebounding after moving sideways over recent weeks as renewed expectations of policy support and stronger-than-expected economic signals from China lifted market sentiment. The upward move was largely driven by China’s manufacturing sector expanding at its fastest pace in about a year, indicating a pickup in industrial demand. Optimism was further supported after the People’s Bank of China signaled it would continue with accommodative monetary policies, fueling expectations of additional stimulus measures. However, gains were capped by elevated inventory levels at Chinese ports, which remain near historic highs. At the same time, other steelmaking inputs moved lower. Prices of coking coal and coke declined, pressured by easing concerns over global energy supply disruptions amid indications that tensions involving Iran could de-escalate.

Gasoline Rises as Markets Gauge Iran Peace Prospects

US gasoline futures rose above $3.20 per gallon on Wednesday, following a brief decline in the previous session, as markets weighed the certainty of signs of de-escalation in the Middle East conflict. President Trump said the US could withdraw from Iran within two to three weeks and suggested a formal deal with Tehran is not required for the conflict to end. Markets remained cautious, however, as he oscillated between signaling a near-term agreement and warning of potential escalation. At the same time, additional US troops arrived in the region, and Tehran said no peace talks were underway but indicated it is ready to end the war if its conditions are met. Meanwhile, gasoline posted a historic 30% monthly surge in March, driven by a broader supply shock from disruptions in the Strait of Hormuz, through which roughly 20% of global oil flows have been nearly halted since the war began.

Silver Extends March Sell-Off

Silver slipped to around $74 per ounce on the first trading day of April, extending its sharp monthly sell-off of more than 20% in March. This marked the steepest decline since September 2011, and silver now trades nearly 40% below January’s record highs, reflecting inflation concerns amid disrupted energy markets and prompting a hawkish shift by investors and central banks. Traders have abandoned expectations of US rate cuts in 2026, reversing pre-war forecasts of two cuts. Meanwhile, markets briefly steadied early in the session as hopes of easing Middle East tensions emerged. President Trump indicated that the US had largely achieved its military objectives and would leave other nations to manage issues in the Strait of Hormuz. This followed Iranian state media citing President Masoud Pezeshkian, who said the Islamic Republic is ready to end the war if its conditions are met.

Gold Rises as Middle East Tensions Ease, Upside Limited

Gold prices rose to around $4,700 per ounce on Wednesday amid signs of de-escalation in Middle East tensions, which could lead to lower oil prices and ease concerns over further central bank rate hikes. President Donald Trump told aides he is willing to end the war against Iran even if the Strait of Hormuz remains largely closed, while regional reports suggested Iran’s President Masoud Pezeshkian may consider ending the conflict under certain conditions. Still, gains in bullion remained limited as easing geopolitical risks reduced safe-haven demand, while a firm US dollar and elevated Treasury yields continued to weigh on non-yielding assets. In March, gold plunged more than 13%, marking its steepest monthly drop since October 2008, and remains nearly 19% below its record highs set in late January. Traders are now closely watching upcoming US economic data and signals from the Federal Reserve for further direction on interest rate expectations.

Baltic Dry Index at Near 3-Week Low, Posts Monthly Loss

The Baltic Exchange’s dry bulk freight index, which monitors rates for ships carrying dry bulk commodities, was down for a second session on Tuesday, falling 1.1% to a near three-week low of 1,995 points. The capesize index, which typically transport 150,000-ton cargoes including iron ore and coal, also retreated for a second day, slumping 1.9% to a near one-week low of 2,947 points; and the supramax index eased 1 point, or 0.1%, to 1,202 points. Conversely, the panamax index, which usually carry 60,000 to 70,000 tons of coal or grain, edged up 0.1% to 1,744 points. The benchmark index recorded a 12.2% decline in March, its first month of losses this year.

Upside Momentum in Palm Oil Continues as April Begins

Malaysian palm oil futures hovered above MYR 4,850 per tonne on the first trading day of a new month, extending gains for a fifth straight session and reaching their highest level since December 2024. Strength came from firmer edible oil prices in Dalian and Chicago markets, alongside stronger crude ahead of U.S. President Trump’s address on Iran. The upside was further reinforced after Indonesia, a top producer, said it will raise its mandatory biodiesel blending rate to 50% (B50) from 40%, starting July 1. In China, another main consumer, factory activity expanded for a fourth consecutive month in March, though growth slowed, according to a private survey. However, gains were capped by a stronger ringgit and expectations of softer demand in top buyer India, with March imports estimated at 680,000 tonnes, down from 847,689 tonnes in February. Meanwhile, EU palm oil imports for the 2025/26 season beginning July slipped 2% year-on-year to 2.14 million tonnes, European Commission data showed.

ROTW UPDATES

Equity indices in the Asia-Pacific region ended Tuesday on a mostly lower note with South Korea’s Kospi (-4.3%) falling to its lowest level since early February while India’s markets were closed for a holiday.

- Japan’s Nikkei: -1.6%,

- Hong Kong’s Hang Seng: +0.2%,

- China’s Shanghai Composite: -0.8%,

- India’s Sensex: CLOSED,

- South Korea’s Kospi: -4.3%,

- Australia’s ASX All Ordinaries: +0.3%.

In news:

- Japan’s Tokyo CPI for March decelerated to 1.7% from 1.8%, but multiple companies have indicated plans for price hikes, suggesting that inflation will reaccelerate in the April reading.

- China’s liquor giant Kweichow Moutai also announced price hikes.

- China’s official Manufacturing (50.4) and Non-Manufacturing PMI (50.1) readings returned to expansion in March.

- South Korea is planning an extra budget of KRW26.2 trln to offset the impact of the war with Iran.

In economic data:

- China’s March Manufacturing PMI 50.4 (expected 50.1; last 49.0) and Non-Manufacturing PMI 50.1 (expected 49.9; last 49.5)

- Japan’s February Retail Sales -0.2% yr/yr (expected 0.9%; last 1.8%), February Industrial Production -2.1% m/m, as expected (last 4.3%), February Unemployment Rate 2.6% (expected 2.7%; last 2.7%), March Tokyo CPI 1.4% yr/yr (last 1.6%) and March Tokyo Core CPI 1.7% yr/yr (expected 1.8%; last 1.8%). February Housing Starts -4.9% yr/yr (expected -4.5%; last -0.4%) and Construction Orders 42.7% yr/yr (last 5.7%)

- South Korea’s February Retail Sales 0.0% m/m (last 2.9%). February Industrial Production 5.4% m/m (expected 1.8%; last -2.4%); -2.2% yr/yr (expected 6.0%; last 6.8%). February Service Sector Output 0.5% m/m (last -0.2%)

- India’s Q3 trade deficit $87.40 bln (last deficit of $93.60 bln)

- Singapore’s February Bank Lending SGD893.6 bln (last SGD887.5 bln)

- Australia’s March Private Sector Credit 0.6% m/m, as expected (last 0.5%) and March Housing Credit 0.6% m/m (last 0.6%)

- New Zealand’s March ANZ Business Confidence 32.5 (last 59.2)

Major European indices trade in the green amid reports that President Trump is willing to end the war with Iran without reopening the Strait of Hormuz.

- STOXX Europe 600: +0.9%,

- Germany’s DAX: +1.2%,

- U.K.’s FTSE 100: +1.0%,

- France’s CAC 40: +0.6%,

- Italy’s FTSE MIB: +0.9%,

- Spain’s IBEX 35: +1.1%.

In news:

- Eurozone’s CPI accelerated to 2.5% yr/yr from 1.9% in the flash reading for March.

- The U.K. reported in-line growth for Q4 (0.1% qtr/qtr) while France’s Consumer Spending (-1.4% m/m) decreased more than expected in February.

- European Central Bank policymaker Muller said that it is probable that rates will have to rise in the coming quarters while policymaker Kazimir said that the central bank will need to act decisively if the Iran war drags on.

- Germany’s Economic Institutes lowered their domestic growth outlook for 2026 to 0.6% from 1.3% while the forecast for 2027 was reduced to 0.9% from 1.4%.

- The inflation forecast for 2026 was increased to 2.8% from 2.0% while the outlook for 2027 was increased to 2.8% from 2.3%.

In economic data:

- Eurozone’s flash March CPI 1.2% m/m (last 0.6%); 2.5% yr/yr (expected 2.6%; last 1.9%). March Core CPI 0.8% m/m (last 0.8%); 2.3% yr/yr (expected 2.4%; last 2.4%)

- Germany’s February Retail Sales 0.7% yr/yr (expected 1.0%; last 0.9%). February Import Price Index 0.3% m/m (expected 0.7%; last 1.1%); -2.3% yr/yr (last -2.3%). March Unemployment Change 0 (expected 2,000; last 1,000) and March Unemployment Rate 6.3%, as expected (last 6.3%)

- U.K.’s Q4 GDP 0.1% qtr/qtr, as expected (last 0.1%); 1.0% yr/yr, as expected (last 1.2%). Q4 Business Investment -2.5% qtr/qtr (expected -2.7%; last 1.1%), Q4 Current Account deficit GBP18.4 bln (expected deficit of GBP24.0 bln; last deficit of GBP10.7 bln). March Nationwide HPI 0.9% m/m (expected 0.0%; last 0.3%); 2.2% yr/yr (last 1.0%). Q4 Business Investment 2.0% yr/yr, as expected (last 3.5%)

- France’s flash March CPI 0.9% m/m, as expected (last 0.6%); 1.7% yr/yr (expected 1.6%; last 0.9%). February PPI -0.2% m/m, as expected (last 0.5%); -2.4% yr/yr (last -2.3%). February Consumer Spending -1.4% m/m (expected -0.3%; last 0.4%)

- Italy’s flash March CPI 0.5% m/m (expected 0.6%; last 0.7%); 1.7% yr/yr (last 1.5%). January Industrial Sales -0.3% m/m (last 0.6%); -1.0% yr/yr (last 3.5%) o Spain’s January Current Account surplus EUR2.73 bln (last surplus of EUR1.80 bln)

U.S. ECONOMIC UPDATES

- January FHFA Housing Price Index 0.1% (Briefing.com consensus 0.0%); Prior was revised to 0.3% from 0.1%

- January S&P Case-Shiller Home Price Index 1.6% (Briefing.com consensus 1.3%); Prior was revised to 1.9% from 1.4%

- March Chicago PMI 52.8 (Briefing.com consensus 54.8); Prior 57.7

- March Consumer Confidence 91.8 (Briefing.com consensus 88.0); Prior was revised to 91.0 from 91.2

- The key takeaway from the report is that the headline numbers don’t convey any abject concern among consumers about the Iran war, yet that concern showed up in higher 12-month inflation expectations, which jumped to 6.2% from 5.5% in February, marking the highest level since August 2025.

- February JOLTs – Job Openings 6.882 mln (Briefing.com consensus 6.795 mln); Prior was revised to 7.240 mln from 6.946 mln

US Crude Oil Inventories Surges More-Than-Expected

US crude oil inventories rose by 10.263 million barrels in the week ended March 27th 2026 the most in many weeks following a 2.3 million barrel increase in the previous week and compared to expectations of a 1.3 million barrel decline. Meanwhile gasoline inventories fell by 3.209 million barrels reversing a 500,000 barrel increase in the previous period. Distillate stockpiles which include diesel and heating oil decreased by 1.04 million barrels following a 1.4 million barrel gain in the previous period.

Dallas Fed Business Activity Contracts Most in 11 Months

The general business activity index published by the Federal Reserve Bank of Dallas plummeted by 10.1 points from the previous month to -13.3 in March of 2026, reflecting the largest magnitude of pessimism since April of the previous year. Revenues grew at a softer pace (1.3 vs 4.1 in February). The drop in the index coincided with a sharp increase in input prices (24.4 vs 22.4) due to the surge in global energy prices after the outbreak of war in the Middle East, while the drop in client’s acquisition power pressured selling price growth (4.9 vs 8.3). Looking ahead, the company outlook index dropped by 7.5 points to -9.9.

US Gas Prices Surge in March Amid Middle East War

US gasoline prices soared in March 2026, with the EIA reporting an average of $3.638 per gallon ($0.96 per liter), the highest since September 2023. In addition, AAA data showed the national average hitting $4.02 per gallon by month-end, topping $4 for the first time since 2022, as the Middle East conflict disrupted global oil markets. Prices at the pump jumped by $1 per gallon in just one month following the US-Israel offensive against Iran, marking a 34.7% increase from February’s $2.98. This monthly surge exceeds even the spikes after Hurricane Katrina (2005) and Russia’s 2022 invasion of Ukraine, making it the sharpest rise in decades.

US Job Quits Fall to 2020-Lows

The number of job quits in the US fell slightly to 2.974 million in February 2026 from the downwardly revised 3.131 million in January and below 3.153 million a year ago. It was the lowest reading since August 2020. The number of quits decreased in accommodation and food services (-119,000), wholesale trade (-35,000), and federal government (-6,000), but rose in nondurable goods manufacturing (+21,000). The quits rate, a metric that measures voluntary job leavers as a proportion of total employment, eased to 1.9% in February from 2% previously. Regionally, job quits decreased in the West (-71,000), the Northeast (-62,000), the South (-14,000) and the Midwest (-11,000)-

US Job Openings Below Forecasts

Job openings in the US fell by 358,000 to 6.882 million in February 2026, below market expectations of 6.92 million. The number of job openings decreased in accommodation and food services (-211,000) and in mining and logging (-12,000). Regionally, openings fell in the Northeast (-110,000), the South (-160,000), the Midwest (-58,000), and the West (-19,000). Meanwhile, hires decreased to 4.8 million, and total separations changed little at 5.0 million. Within separations, quits (3.0 million) were little changed while layoffs and discharges (1.7 million) were unchanged.

US House Prices Edge Up 0.1%: FHFA

US single-family home prices backed by Fannie Mae and Freddie Mac increased 0.1% in January 2026, in line with market expectations after a 0.3% rise in December. For the nine census divisions, home price changes ranged from -0.7% in the West South Central division to +1.7% in the East South Central division. Year-over-year, house prices rose 1.6% in December. The 12-month changes ranged from -0.8% in the West South Central division to +4.4% in the East North Central division.

US Home Price Growth Slows to Weakest Since 2023

The S&P Cotality Case-Shiller 20-City Home Price Index rose 1.2% year over year in January 2026, down from 1.4% in December and below market expectations of 1.3%. This marked the weakest annual growth since July 2023, underscoring the continued cooling in the US housing market. For the eighth straight month, home price appreciation lagged consumer inflation, pushing real home values slightly lower compared to a year ago. New York led gains with a 4.9% annual increase, followed by Chicago (4.6%) and Cleveland (3.6%), while Tampa saw the largest decline (-2.5%). On a monthly basis, prices dipped 0.1% before seasonal adjustment but ticked up 0.2% after, signaling a market in stabilization mode, neither rebounding nor crashing.

- President Trump told advisors he is willing to end Iran war even if Strait of Hormuz remains largely closed. WSJ

- President Trump says “All of those countries that can’t get jet fuel because of the Strait of Hormuz, like the United Kingdom, which refused to get involved in the decapitation of Iran, I have a suggestion for you: Number 1, buy from the U.S., we have plenty, and Number 2, build up some delayed courage, go to the Strait, and just take it.” Truth Social

- Iran’s leadership is struggling to coordinate. NY Times

- Bloomberg reporter says “The Pakistani and Chinese foreign affairs ministers have met today in Beijing, according to Chinese state media. The meeting comes as rumors abound that Beijing could play a role as “guarantor” of any US-Iran deal.”

- Foreign central banks cut Treasury holdings since Iran war. FT

- U.S. average gas prices reach $4.00 per gallon, highest since 2022, AAA says

- Pentagon Secretary Pete Hegseth’s broker attempted to make a large investment in defense companies ahead of Iran war. FT

- Dubai Media Office says “Authorities in Dubai confirm their response to an incident involving a drone affecting a Kuwaiti oil tanker in Dubai waters (Anchorage “E”), with no injuries reported”

- Eurozone’s flash March CPI 1.2% m/m (last 0.6%); 2.5% yr/yr (expected 2.6%; last 1.9%). March Core CPI 0.8% m/m (last 0.8%); 2.3% yr/yr (expected 2.4%; last 2.4%)

- President Trump eyes forcing Congressional special session to end DHS funding lapse, according to NYPost

- Strait of Hormuz traffic edges higher as Iran allows limited friendly ship transits, according to Bloomberg

- White House position remains the same; U.S. says diplomatic negotiations are ongoing, but also preserving military options; Iran Foreign Minister says he is receiving direct messages from U.S. Special Envoy Steve Witkoff, but Iran says that this doesn’t court as “talks” or “negotiations” – CNBC

- Virtus Minerals to acquire Chemaf, according to WSJ

- USS George H.W. Bush deploying to the Middle East, according to WSJ

EARNINGS SEASON AND GUIDANCE

- AT&T (T) reiterates FY26 guidance

- Constellation Energy (CEG) provides guidance in slide presentation; sees FY26 EPS in line

- FactSet (FDS) beats by $0.07, beats on revs; raises FY26 EPS in-line, revs in-line

- Hershey Foods (HSY) reaffirms FY26 guidance ahead of Investor Day today

- Hershey Foods (HSY) releases Investor Day presentation; Strong visibility to consistently deliver Long-Term Algorithm (reaffirmed FY26 guidance before the open)

- Inogen (INGN) reaffirms FY26 revenue guidance

- McCormick (MKC) beats by $0.07, beats on revs; reaffirms FY26 EPS guidance, revs guidance

- NervGen Pharma (NGEN) reports full year 2025 financial results and provides business updates

- Phreesia (PHR) misses by $0.04, reports revs in-line; guides FY27 revs below consensus

- Progress Software (PRGS) beats by $0.03, reports revs in-line; guides Q2 EPS above consensus, revs in-line; guides FY26 EPS above consensus, revs in-line

- Snowflake (SNOW) reaffirms Q1/FY27 and FY27 guidance

- SunPower (SPWR) filed to delay its 10-K; Expects significant changes

- TD Synnex (SNX) beats by $1.42, beats on revs; guides Q2 EPS above consensus, revs above consensus

- Vale S.A. (VALE) informs on estimates update including potential contribution of its subsidiary Vale Base Metals

- Virgin Galactic (SPCE) announces fourth quarter and full year 2025 financial results and provides business update

2026 APR 01

Pre-Market: CALM CAG LW MSM UNF

After-Hours: PENG

THE WEEK AHEAD

WEEK 13: MONDAY TO FRIDAY, MARCH 30 to APRIL 03

According to the PTSD*, Week 14 has FOUR trading days and is the FIRST trading week in April 2026. The next Market Holiday is on FRIDAY APR03. Seasonally, Week 14 has a Bearish-to-Flat outlook, leading to a more positive Week 15. outlook with Risk-On sentiment, at least on the 15-year cycles. April is the last of the “6 months of bullishness” on the SPX.

We also need to keep in mind that with the current POTUS, seasonals can easily go out of whack.

*PTSD – Penguin Trader Seasonal Data.

BENCHMARK INDICES (21-YEAR AVERAGE)

The Stock Trader’s Almanac’s stats for the Benchmark Indices for 2026 APRIL 01 of Week 13 over a 21-year average are:

- Dow Jones (DJIA): Somewhat Bullish 66.7%

- S&P 500 (SPX): Somewhat Bullish 66.7%

- NASDAQ (COMP): Somewhat Bullish 61.9%

- *Russells 2000 (RUT): Somewhat 66.7%

*The RUT is not listed in the STA; several penguins with a slide ruler calculated the 21-year average.

BENCHMARK INDEX ETFs

The Penguin Trader Seasonal Data (PTSD) stats for the Benchmark Index ETFs for 2026 APRIL 01 of Week 13 over a 15-year average are:

- DIA – (15yr Avg): Somewhat Bullish 53.3%

- SPY – (15yr Avg): Somewhat Bullish 60.0%

- QQQ – (15yr Avg): Somewhat Bullish 60.0%

- RUT – (15yr Avg): Somewhat 53.3%

ECONOMIC DAY AHEAD

For USA’s upcoming economic calendar features:

- 7:00 ET: Weekly MBA Mortgage Index (prior -10.5%)

- 8:15 ET: March ADP Employment Change (Briefing.com consensus 42,000; prior 63,000)

- 8:30 ET: February Retail Sales (Briefing.com consensus 0.5%; prior -0.2%) and Retail Sales ex-auto (Briefing.com consensus 0.3%; prior 0.0%) · 9:45 ET: Final March S&P Global U.S. Manufacturing PMI (prior 52.4)

- 10:00 ET: March ISM Manufacturing (Briefing.com consensus 52.3%; prior 52.4%)

- 10:30 ET: Weekly crude oil inventories (prior +6.93 mln)

ANALYSIS

Yes – I think APR01 might be “Somewhat Bullish”. Profit takers will be jumping in, and the folks caught with their pants down in their shorts (pun intended) will be jumping out. I do not expect another 2%-3% upswing, but it could happen with more POTUS prodding.

COMMENTARY

On the home front:

One of my VS got its profit trigger just BMC, I woke up happy.

The other tiers in the ladder are queueing up for their triggers.

March ended with a down. The Samurai called in months ago in one of these sessions with us. The December Low indicator is bearish. We are also in the current POTUS’s 2nd year in his term.

Stay Hedged – My Penguin Friends

(Excerpts from briefing.com, tradingeconomics.com, financialscents.com, factset.com, finviz.com, marketwatch.com, etrade.com, yahoo.com, tigerbrokers.com, tradingview.com, tradingcentral.com, theedgemalaysia.com, sectorspdrs.com, Investopedia.com, and CNBC.com)